-article_image.jpg&w=1920&q=75)

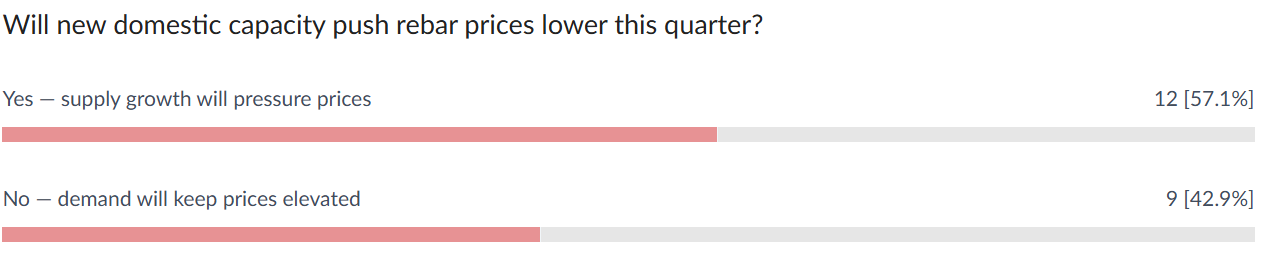

Updates From This Week US Rebar & Wire Rod: High Prices Amidst Import UncertaintyRebar options remain constrained following the aggressive trade actions against Egypt, Vietnam, Bulgaria, and Algeria. South Korea has emerged as a potential supplier to the US; while they previously operated under a strict quota, the 2025 regulatory shifts under Section 232 eliminated those quotas in favor of a 50% ad valorem tariff. Despite this staggering cost barrier, elevated US domestic prices have made South Korean imports commercially viable, and volumes are expected to rise through the first half of 2026. While the US Treasury collects these record tariffs and domestic mills enjoy unprecedented margins, the burden falls on the supply chain. The "metal spread"—the gap between scrap costs and finished rebar—now exceeds $500 per ton, more than double the historical average of roughly $200. These inflated costs are directly impacting construction budgets and downstream businesses at a time of broader economic volatility. The wire rod market faces similar constriction. Countries like Egypt, Algeria, Malaysia and Vietnam are able to ship wire rod to the US without antidumping duties, but they remain wary of "threat of injury" investigations that could abruptly block market access. In North Africa, pricing remains higher than Asian offers. However, as Asian markets show signs of firming, the window for low-priced imports may close. Asian mills have moved away from their previous price floors, though the sustainability of these increases remains a point of contention. Regarding trade litigation, the threshold for imposing duties has shifted; proving actual "material injury" is no longer the sole requirement, as a "threat of injury" now suffices. The International Trade Commission (ITC) is currently finalizing its determination on rebar imports. It will be a landmark conclusion, as the administration must argue that the domestic industry is "threatened" despite recording record profits and maintaining strict allocation for most customers. Importers are caught in a multi-directional squeeze, yet imports remain essential to prevent a major domestic shortage. The only new wire rod capacity in the plan is a new hybrid Hybar mill that will produce rods and rebars, yet the new mill is still several years away from production. Regarding rebar, supply is showing signs of stabilization. As scrap prices cool heading into March, the upward pressure on steel may ease by the third quarter, though buyers remain cautious given the current global turmoil and record-high price levels. Weekly Poll If imports tighten further, will the US face a rebar shortage in 2026? Last Week's Poll Result  🚀 Coming Soon: StaalXneXtThe steel market is evolving. So are we. StaalXneXt is the next phase of the StaalX platform — built to expand access, increase supply visibility, and create smarter connections between buyers and sellers across long products and beyond. Designed for greater transparency and deeper market reach, StaalXneXt will introduce a more dynamic multi-vendor environment — while maintaining the reliability and performance our partners expect. Launching soon. Stay tuned — the next evolution of steel commerce is almost here.  Explore the upgrades at www.staalx.com or get in touch today with websupport@staalx.com to see the difference.  🎧 Missed Episode 18? Catch up now — we break down the Supreme Court’s decision to strike down certain IEEPA tariffs and what this legal reset could mean for steel pricing, imports, and construction costs in 2026. As AI-driven data center construction accelerates while housing remains under pressure, tariff uncertainty adds another layer of volatility. This episode unpacks whether contractors should expect real material cost relief — or prepare for continued recalibration across rebar, wire rod, beams, and reinforcement markets. Listen now on ▶️ YouTube | 🎵 Spotify | 🎙 Apple Podcasts 👉 Follow the StaalX Construction & Steel Podcast for weekly insights on market shifts, freight trends, and sourcing strategies.  From our content partner, SteelOrbis .jpeg) US domestic long steel pricing mixed on sideways March scrap, mill discounts, imports rise Thursday, 26 February 2026 17:30:29 (GMT+3) San Diego US rebar and wire rod markets were mixed this week with domestic rebar markets reported marginally lower while wire rod pricing moved up slightly, market insiders told SteelOrbis. This week’s juxtaposed pricing is the result of continued tight domestic wire rod supply as several mills among them Peoria, Illinois-based Liberty Steel, continue to produce below their rated capacity, helping recent mill price increases for wire rod to gain traction in the marketplace. Rebar markets are steady to slightly down as mills begin to explore the use of limited discounting programs to retain customers in the face of reports of growing imports. Domestic rebar prices on an FOB Midwest mill basis fell $0.50/cwt., this week to on average $47.50-48.50/cwt., ($950-970/nt or $1,047-1,069/mt), off from $48.00-49/cwt., ($960-980/nt or $1,058-1,080/mt), a level where pricing stood unchanged for five previous weeks. “Scrap looks like its going to come in sideways at this point for March, and imports are starting to come in,” reported one US East Coast rebar insider. “Prices are not moving much, but, (new demand) remains very slow out there right now.” “Mills have shown modest [rebar] concessions ($10-30/ton in some cases), largely tied to seasonal inventory management rather than structural weakness,” reported another US Gulf Coast rebar insider. “Scrap price increases over the past three months continue to underpin pricing floors.” And, while rebar prices remain more than 4 percent higher versus the beginning of the year, since February 2025, rebar pricing is up more than 22 percent, mostly on scrap price increases and improved demand from associated AI data center builds and other infrastructure project developments, insiders said. Insiders explained that more output from both North Carolina-based Nucor’s 430,000 ton per year Lexington rebar micro mill, as well as Hybar LLC’s new 700,000 ton per year rebar mill near Osceola, Arkansas, is contributing to renewed discounting from local mills, especially since reports of increased imports continue to be reported to SteelOrbis. “We’re hearing reports that Nucor has offered to match lower import barge pricing for rebar,” said one US Gulf Coast long steel insider. “And, recent wire rod price increases largely have been accepted by the market which is causing wire rod to move a bit up.” On Feb. 11, Nucor announced a $30/ton ($1.50/cwt.) increase in spot wire rod prices, though market acceptance of Nucor’s increase remained limited this week with prices up only about $0.50/cwt. In the US scrap markets, this week’s exclusive SteelOrbis survey of market participants finds both mills and suppliers in agreement that pricing will likely cool off for March and April, following three straight months of steady price increases. “We just got a couple more inches of snow last night and it’s fine,” said one Midwest-based scrap supplier. “I’m hearing sideways for March and possibly down for April,” he said. “I initially expected to see a small bump in March scrap pricing but now it’s all sideways as inflows are starting to pick up from levels we saw about two weeks ago when the weather was a disaster, and our trucks and equipment wouldn’t even start. Now that we’ve gotten through that, inflows are a lot more manageable.” “I think inflows are pretty solid,” reported one US Midwest-based mill scrap buyer. “There is plenty of material being made available.” In the domestic wire rod market, insiders expect wire rod pricing to remain strong near term with additional weekly price increases likely as domestic supply is expected to remain tight and imports limited through the first half of 2026. Spot domestic wire rod prices on an FOB mill basis were assessed with most transactions noted $0.50/cwt., higher at $48.50-49.50/cwt., ($970-990/nt or $1,069-1,091/mt), up from $48.00-49.00/cwt ($960-980/nt or $1,058-1,080/mt), or an average of $48.50/cwt ($970/nt or $1,069/mt), a price level the product has maintained for more than 10 weeks. US import long steel prices steady to up on talk of increased imports, steady to down scrap Thursday, 26 February 2026 22:17:46 (GMT+3) San Diego US import rebar and wire rod pricing was slightly higher this week even as reports continue that long steel imports are likely to continue to rise. This week’s small price bump comes at a time when US scrap prices for March and April are expected to be stable to potentially lower for the first time in more than three months, market insiders told SteelOrbis. The outlook for a break in the ongoing US scrap price rally follows another recent round of domestic mill long steel and structural steel price increase announcements, boosting rebar and wire rod spot prices to levels not seen since late-2022. These price hikes, insiders said, will continue to make room for a limited amount of imports to enter the US markets, mostly from South Korea, even though existing 50 percent Section 232 steel tariffs, long lead times, and strong freight rates could keep volumes on the low side. And while most steel insiders told SteelOrbis imports are likely to creep up as US long steel prices rise, the extent of the import increase remains in contention. “While some suppliers are expecting imports in the first half of 2026 (1H) to fall in the 100,000-150,000 metric ton range, we are expecting to see 1H imports much higher than some anticipate in the 300,000 to 400,000 mt range,” noted one Chicago-based long steel importer. “We’re expecting to see spring and summer import arrivals priced from Korea in the $43.50-44.50/cwt., [$870-890/nt or $959-981/mt] range. However, given current two month lead times for supply contracted today, new imports will not arrive in the US until July or August.” On the US Gulf Coast, import rebar on a loaded truck basis is reported $0.50/cwt., higher at $44.50-45.50/cwt., ($890-910/nt or $981-1,003/mt). US East Coast import rebar pricing was steady to week-ago levels at $45.00-46/cwt., ($900-920/nt or $992-1,014/mt), insiders said. “South Korea remains the primary viable supplier, particularly Hyundai Steel,” noted one US Gulf Coast importer to SteelOrbis. “Volumes are expected to remain limited… with higher FOB offers [around $550/mt] expected to reduce arbitrage opportunities.” In March 2025, Hyundai Steel announced a major $5.8 billion investment to build its first US steel production facility in Donaldsville, La. The new plant, with a stated annual capacity of 2.7 million tons, will produce automotive steel plates for Hyundai and KIA factories in Alabama and Georgia. Groundbreaking is expected to begin early this year with a completion date targeted for 2029. In the weekly import wire rod markets, wire rod mesh on a DDP loaded truck basis is reported at $44.00-45/cwt., ($880-900/nt or $970-992/mt), up $0.50/cwt from one week earlier. “Asian markets remain competitive globally, but US tariffs and freight costs continue to limit penetration,” remarked the US Gulf Coast importer. “Wire rod fundamentals are stable to firm, with domestic pricing cost supported with limited near-term downside risk.” And while importers report selective discounting on domestic merchant bars of $2-4/cwt., ongoing section 232 tariffs have significantly reduced competitiveness of offshore MBQ import offers with pricing noted near $1,200/nt ($60.00/cwt.) on a landed basis. “Buyers that had previously relied on imports are increasingly sourcing domestically or regionally [Mexico where viable].” March US scrap seen mostly sideways on better weather, yard inflows up Thursday, 26 February 2026 22:23:29 (GMT+3) San Diego This week’s exclusive SteelOrbis survey of US scrap market participants finds most still see March scrap pricing sideways, versus week ago calls for sideways to potentially down, as weather continues to improve, likely boosting the flow of scrap into local supply yards, market insiders told SteelOrbis. During the period leading up to the recent February buy-cycle scrap negotiations, record cold temperatures and snow and ice storms across more than 30 states stunted yard scrap inflows while icy roads and frozen rivers reduced the ability to transport prompt scrap to markets. Midwest Ohio Valley shredded scrap prices rose on average $30/gt to $445-450/gt ($452-456/mt). “We’re hearing sideways for March and potentially lower for April,” stated one Detroit-based supplier. “Inflows are starting to really pick up from about 2 weeks ago when the weather was a complete disaster. Now that we’ve gotten through that, inflows are quite a bit more manageable.” “There’s lots of sideways talk for March, maybe even down slightly,” added one Midwest mill scrap buyer. “I think inflows are solid, with plenty of material available.” According to the 6-10 day temperature outlook from the US National Weather Service’s (NWS) Climate Prediction Center, temperatures over the period across much of the US are expected above normal, while portions of the US Northeast could see near-normal to below-normal temperatures. Much of the US, with the exception of the US South, is forecast for above-normal precipitation, with much of the US Southeast forecast for near-normal precipitation during the period. Insiders told SteelOrbis expected moderation of weather to more seasonal norms will allow scrap suppliers and mills more time to build depleted inventory levels ahead of March and later April supply negotiations. Based on a current sideways call for March scrap, US Ohio Valley prime busheling scrap could settle near its $30/gt higher February settlement at $445-452/gt ($452-462/mt), while March shredded material could finish near its $30/gt higher February finish at $445-450/gt ($452-456/mt). In the cut grades, a sideways expectation for P&S scrap near $421-431/gt ($427-437/mt) is likely, following its $20/gt February gain. March HMS, which also rose $20/gt this month, is likely to settle at $385-405/gt ($390-410/mt), scrap insiders told SteelOrbis. In the US Northeast, a current sideways March expectation could yield busheling scrap near $420-420/gt, following its recent $30/gt February gains. Shredded scrap, which also rose $30/gt, could finish near $395-405/gt ($400-410/mt), while P&S and HMS grades, which both saw $20/gt February price increases, could finish near $350-360/gt ($355-365/mt), and $365-380/gt ($370-385/mt), respectively. Do you have any questions? Check out our FAQ!Check out the most frequently asked questions about the service and products of StaalX. We are always here to chat with you in the chat boxes from the site or on the support telephone number below. Contact us websupport@staalx.com or +1 (708) 697-3227 Follow StaalX on |

Need steel? Get an instant quote & save $500 off your first order

Search rebar, wire rod, wire mesh and more on StaalX. Check availability and book reliable delivery nationwide.

For sponsorship opportunities or advertising on StaalX News, contact us at websupport@staalx.com.