-(1)-article_image.jpg&w=1920&q=75)

🚀 It’s Live: Meet StaalXneXt (Beta)StaalXneXt Beta is now live — an invitation-only marketplace built for serious buyers and sellers. Access exclusive supply, unlock hidden inventory, and connect with trusted partners across domestic and global markets. From spot opportunities to future orders — with flexible Net 30 / 60 / 90 payment terms — StaalXneXt gives you the control the traditional market never did.  Explore the upgrades at www.staalx.com or get in touch today with websupport@staalx.com to see the difference. Updates From This Week The US Rod Buyer’s PredicamentWhile walking the halls of the massive Wire and Tube show in Duesseldorf this week, it is impossible to ignore the irony: hundreds of world-class wire rod producers are aggressively promoting their mills, yet the vast majority are effectively barred from the US market. Decades of accumulated anti-dumping (AD) and countervailing duty (CVD) orders have created a fortress around the US. Many producers have never shipped a single pound of steel to American shores—some weren't even in business when the original duties were established—yet they remain locked out. This is due to the "All Others" category in US trade law, which assigns high, prohibitive duties to any mill not individually investigated, making entry a financial impossibility. These barriers rarely fall. The five-year "Sunset Review" process, designed to phase out old duties, almost never results in an actual sunset. Just this year, we saw 20-year-old orders on Brazilian rod reaffirmed yet again, ensuring that trade barriers continue to stack up like cordwood. A Chilling Effect on Supply Last week, US domestic producers filed yet another countervailing investigation, alleging Algerian subsidies for their rod exports to the US. Surprisingly Algerian rod hasn't been a major factor in the US market. They haven't entered a pound of rods since June 2025 and haven't been a major importer even before that.

The aggressive trade atmosphere was further punctuated recently by the final affirmative dumping and subsidy determinations on rebar from Algeria, Egypt, and Vietnam. While these specific cases targeted rebar, the "spooked" reaction is palpable in the wire rod sector. Egypt, for instance, has effectively vanished from US import statistics, wary of being the next target. This lack of options is strangling US rod-consuming industries. While domestic producers benefit from the lack of competition in the short term, they risk presiding over a shrinking consuming industry. A weakened downstream wire industry eventually leaves rod producers with no one to sell to. Despite the wave of new "greenfield" steel projects in the US, wire rod has seen almost zero interest from investors or domestic steel giants. The Summer Squeeze

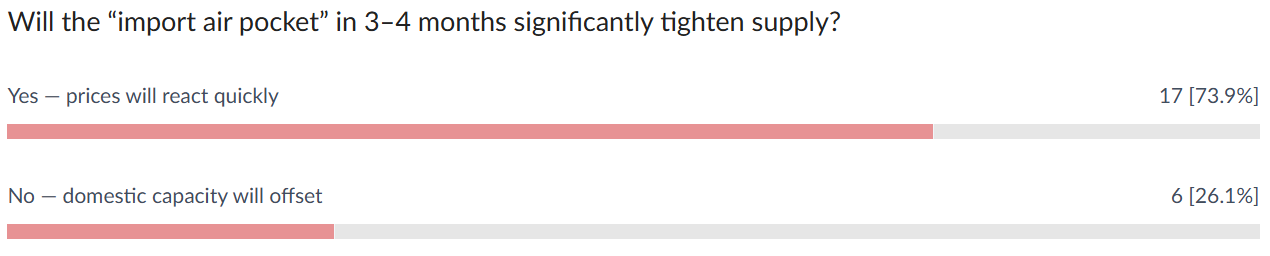

Currently, viable import options are largely narrowed down to Vietnam and Malaysia. Even these are becoming "expensive" alternatives as ocean freight rates climb and domestic demand in Southeast Asia rises. To compound the crisis, two domestic rod mills reported significant production outages this week with no firm restart dates. Rod buyers are now facing a brutal choice: lock in expensive imports for August/September arrival now, or gamble on an increasingly unpredictable domestic supply chain. For those in the rebar market, the situation is a mirror image, though slightly mitigated by the arrival of two new domestic mills and plenty of imports in the first half of the year. For rod buyers, however, the name of the game is survival in a market of dwindling choices. Weekly Poll Are current US trade protections helping or hurting the rod market? Last Week's Poll Result   🎧 Missed Episode 21? Catch up now — we break down the contractor’s dilemma as rising costs collide with shifting trade policy. From tariffs and global supply constraints to logistics bottlenecks, this episode explains what’s really driving cost pressure across steel and construction. Listen now on ▶️ YouTube | 🎵 Spotify | 🎙 Apple Podcasts 👉 Follow the StaalX Construction & Steel Podcast for weekly insights on market shifts, freight trends, and sourcing strategies.  From our content partner, SteelOrbis .jpeg) US domestic long steel prices steady to down on enhanced supply availability, oil price slump Thursday, 09 April 2026 16:55:47 (GMT+3) San Diego US long steel prices were steady to slightly lower for a second week, amid reports that US mills had made more rebar supply available even as US oil prices slumped following the April 7 two-week ceasefire announcement between the US and Iran, insiders told SteelOrbis. Among other key issues, the US-Iran ceasefire calls for safe passage of all shipping through the contested Strait of Hormuz, where 20 percent of the world’s oil moves. On April 8, US benchmark West Texas Intermediate (WTI) crude oil traded for May delivery at $95 per barrel (/bbl), a one-day drop of more than 16 percent following the announcement. And, while oil prices were down sharply, WTI prices remain nearly 42 percent higher than they were before hostilities started Feb. 28. “The Iran-US ceasefire has cooled things off a little,” remarked one US Midwest long steel insider. “Transportation costs are improving everywhere as a result of lower global oil prices.” He continued, “The recent news of a ceasefire has been good, and oil prices are declining. The hope is that this war will end soon, and markets will move back to where they were before the hostilities began.” And, while US domestic long steel markets remain largely insulated from potential hostilities in the Middle East, the resulting increases in global oil prices has caused US freight and transportation surcharges to rise, some say as much as 20-30 percent. SteelOrbis market insiders claimed higher diesel pricing alone was expected to boost US delivered finished steel prices by $0.50-1.00 a ton. In the domestic rebar market, Midwest rebar on an FOB mill basis sold on average $46.50-47.50/cwt., ($930-950/nt or $1,025-1,047/mt), off $0.50/cwt., from the $47.00-48/cwt., ($940-960/nt or $1,036-1,058/mt), reported one week earlier. Insiders said current rebar lead times remain improved at 4-6 weeks as more productive capacity is made available from Nucor, Lexington, as well as Hybar Steel. “In the US, we’re seeing more supply availability,” the Midwest insider added. “Hybar steel in Arkansas is now offering domestic rebar supply at $44.00-45.00 per cwt., which is bringing average spot values down a bit versus a week ago.” “We’re not seeing much change in pricing this week,” reported still another US East Coast rebar insider to SteelOrbis. “Everyone’s waiting for demand to come back, so things remain pretty quiet.” In the domestic wire rod markets, insiders told SteelOrbis prices were stable for a fourth week, though reports of tight supply persist as supply from Peoria, Illinois-based Liberty Steel’s 700,000-ton wire and rod plant remains limited, they said. Average SteelOrbis spot prices for wire rod mesh on an ex-mill Midwest basis remain flat at $49.00-50.00/cwt., ($980-1,000/nt or $1,080-1,102/mt). “Wire rod continues to show relative strength versus rebar, with tighter supply and higher sensitivity to cost inflation,” said another US Gulf Coast long steel insider. “This segment is likely to move higher first.” In the domestic ferrous scrap market, weekly SteelOrbis surveys indicate April Midwest scrap traded sideways for prime grades and at a $20/gt discount to March values for cuts and shredded scrap grades, insiders said. Discussions of potential $30/gt discounts for cuts and shredded grade scrap discounts to March pricing in the US South remained unconfirmed at press time. US import long steel prices steady, near-term imports unlikely to pressure price levels Thursday, 09 April 2026 22:02:13 (GMT+3) San Diego For a third week, import long steel prices were reported steady, following an earlier Iran war-related freight and fuel adjustment higher, amid new reports that increased rebar supply at US Gulf Coast ports was unlikely to cause significant price disruptions due to ongoing 50 percent steel import tariffs and steady to lower domestic long steel pricing, market insiders told SteelOrbis this week. Even as a fragile April 7 US-Iran war ceasefire continued on April 9, insiders reported limited new shipments of Korean rebar arriving at US Gulf Coast ports, some of which was expected to offload at Corpus Christie, Tx., Houston, Tx., and New Orleans, La. In addition to current arrivals, more ships remain enroute from Korea, insiders said. “We expect there to be additional spot supply available probably next month,” added one US Gulf Coast rebar importer. “Even if the supply is sold to distributors, it will land at $44-45/cwt. ($880-900/nt or $970-992/mt). “There are more than a few shipments to the US currently on the water,” remarked another US Midwest long steel importer. “Once they arrive, we don’t expect them to have a significant impact on pricing, because of steel tariffs and because domestic and import pricing currently are so close (about $10/ton). Recent gaps in Gulf Coast rebar supply have been filled.” On the US Gulf Coast, import rebar on a loaded truck basis remains flat for a sixth week following an earlier $0.50/cwt., freight-related price adjustment to $44.50-45.50/cwt., ($890-910/nt or $981-1,003/mt). US East Coast import rebar pricing on a loaded truck basis also was stable to week-ago levels at $45.00-46/cwt., ($900-920/nt or $992-1,014/mt). Domestic rebar traders told SteelOrbis this week that increased output from two key US mills, Nucor, Lexington, Ky., and Hybar Steel, in Arkansas, was preventing US rebar prices from rising to the point where import material had much room to be competitive. This week, domestic rebar pricing fell for a second time in as many weeks by $0.50/cwt., to $46.50-47.50/cwt., ($930-950/nt or $1,025-1,047/mt) on an FOB mill basis, further lowering the attractiveness of import material, they said. In the wire rod markets, import wire rod mesh on a DDP loaded truck basis USG remained flat at $46.50-47.50/cwt., ($930-950/nt or $1,025-1,047/mt). “Wire rod pricing remains stable week over week, though could be subject to upward price pressure from recent freight volatility,” remarked one US Gulf Coast long steel insider. “Wire rod continues to show relative strength versus rebar, with tighter supply and higher sensitivity to cost inflation.” On April 9, US benchmark West Texas Intermediate crude oil (WTI) futures for May delivery on the New York Mercantile Exchange (NYMEX) traded at $102 per barrel (/bbl), up more than 3 percent on the day, amid renewed geopolitical tension in the Middle East, specifically, with regard to Israeli missile attacks on Hezbollah positions in Lebanon ,and continued low volume of shipping through the Strait of Hormuz. Prior to the conflict, WTI oil prices on NYMEX were about $67/bbl. US April domestic scrap prices settle -$20/gt on obsoletes, sideways on primes, in most markets Friday, 10 April 2026 22:51:13 (GMT+3) San Diego Ferrous scrap prices began to settle late this week, with secondary grades in the Midwest falling by $20/gt ($20.3/mt) from March settled prices and prime grades remaining sideways, aligned with SteelOrbis’s previous projections. In Chicago, the price of #1 busheling remained at $450/gt ($457.2/mt) delivered consumer while shredded fell by $20/gt ($20.3/mt) to $430/gt ($436.9/mt) delivered, finally separating the grades by $20/gt, the usual spread between the two. HMS I in Chicago fell $20/gt ($20.3/mt) to $370/gt ($375.9/mt) delivered. In Detroit, it was a similar story, with #1 busheling remaining at $455/gt ($462.3/mt) while shredded dropped $20/gt ($20.3/mt) to $430/gt ($436.9/mt) delivered. The disparity that was expected between #1 busheling and shredded material was expected for several months now. In March, US mills left all prices unchanged and postponed the matter. #1 busheling and shredded prices had traded at the same level for four months. For example, in Pittsburgh, the prices of both grades stood only $3/gt ($3/mt) apart since January, and in December, the difference was of only $7/gt ($7.1/mt). Shredded appreciated more rapidly during the winter months, as shredders and other related equipment were particularly susceptible to downtime during the harsh weather, as they endured the elements. #1 busheling, on the other hand, was less susceptible to those effects. In the southern US, particularly Texas, some buyers tried to push cut grades down by $25/gt ($25.4/mt) to offset scheduled maintenance downtime, while others followed the Midwest trend. In Dallas, the price of HMS I dropped by $22/gt ($22.3/mt) to $443/gt ($450.1/mt) delivered consumer while shredded fell by $20/gt ($20.3/mt) to $400/gt ($406.4/mt) delivered. For May, some sellers hope the scrap market could bounce back due to rising prices for finished steel. The price of hot-rolled coil continues to climb, rising by $5/nt ($5.5/mt) in the past week to $1,040/nt ($1,146/mt) FOB mill this week. Yet there are still a number of scheduled maintenance shutdowns for May (although not as many as in April), and historically, both in 2024-2025 have fallen in March and not recovered for the entire year in both cases. Do you have any questions? Check out our FAQ!Check out the most frequently asked questions about the service and products of StaalX. We are always here to chat with you in the chat boxes from the site or on the support telephone number below. Contact us websupport@staalx.com or +1 (708) 697-3227 Follow StaalX on |

Need steel? Get an instant quote & save $500 off your first order

Search rebar, wire rod, wire mesh and more on StaalX. Check availability and book reliable delivery nationwide.

For sponsorship opportunities or advertising on StaalX News, contact us at websupport@staalx.com.