What Happens There, Effects Here

Domestic rebar and wire rod prices have remained relatively stable since the conflict with Iran began, yet buyers feel the sting of surging logistics costs. Rising diesel prices and record-level tender rejections in the flatbed sector are driving up the delivered price for all varieties of steel and construction materials.

Tender rejection rates for flatbeds recently surged to over 41%—one of the highest levels ever recorded and the most significant spike since pandemic-era disruptions. This trend is driven not by a sudden boom in demand, but by severe capacity constraints and carrier exits, which are tightening the market from the supply side.

The volatility began with a rapid ascent in diesel prices, which jumped to a nationwide average of $5.16 per gallon from just under $3.90 prior to the strikes in Iran. This triggered a cascade of contract cancellations in an already strained trucking sector, as carriers began prioritizing lucrative spot-market loads over contracts quoted only days earlier. While fuel costs were the primary catalyst, this "capacity crunch" was long expected due to mounting pressure on non-domiciled Commercial Driver’s Licenses (CDLs). The implementation of Dalilah’s Law at the federal level has further tightened capacity by cracking down on CDL issuances and enforcing stricter eligibility requirements.

In the meantime, domestic mill increases continue for both flat and select long products. Last week, Nucor increased structural merchant bar prices (4" and over) by $2 to $3/cwt. Flat-rolled prices also continue their climb; Nucor recently announced another $10/short ton increase, bringing Hot Rolled Coil (HRC) to $1,025/short ton. Notably, HRC prices are once again trading at a premium over rebar, a reversal of the trend often seen in flat vs. long product spreads.

The pricing trend for all steel products remains bullish. Imports are becoming costlier as ocean freight, inland transportation, and general steelmaking costs continue to rise. The primary concern now is a potential "consumption collapse." There is a growing fear that steel demand may buckle under the combined weight of record-high prices and a cooling construction sector. While data center projects are currently keeping construction spending buoyant, even that sector is showing signs of fatigue as the American power grid approaches its capacity limits.

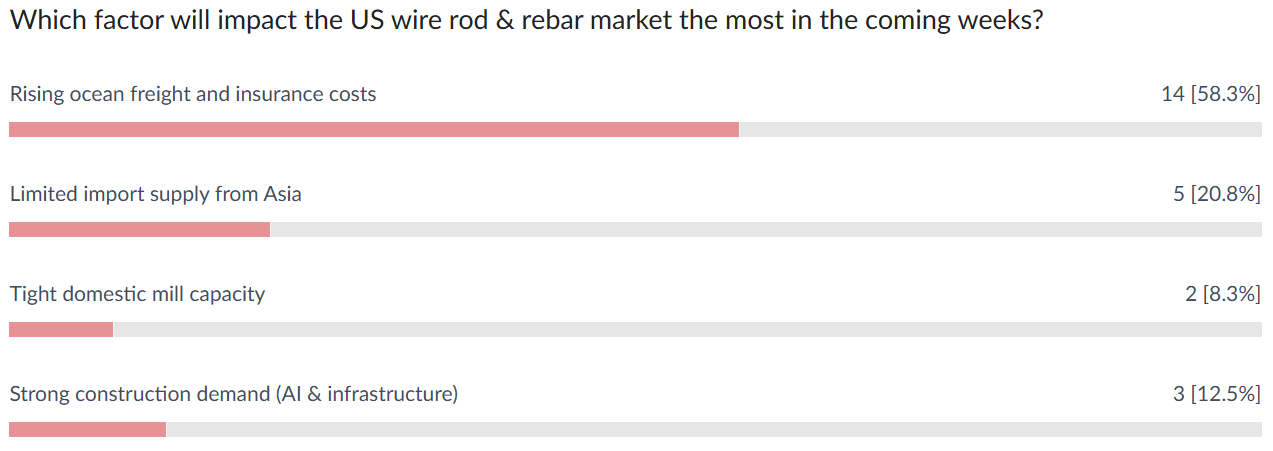

What’s the biggest risk to the steel market right now?

🚀 Coming Soon: StaalXneXt

The steel market is evolving. So are we.

StaalXneXt is the next phase of the StaalX platform — built to expand access, increase supply visibility, and create smarter connections between buyers and sellers across long products and beyond.

Designed for greater transparency and deeper market reach, StaalXneXt will introduce a more dynamic multi-vendor environment — while maintaining the reliability and performance our partners expect.

Launching soon.

Stay tuned — the next evolution of steel commerce is almost here.

🎧 Missed Episode 19? Catch up now — we break down how the escalating Iran conflict could impact U.S. construction costs, steel pricing, and global supply chains in 2026.

From rising oil and freight costs to disruptions around the Strait of Hormuz, the episode explores what contractors, distributors, and steel buyers should watch in the months ahead.

From our content partner, SteelOrbis US domestic long steel prices steady, April scrap balanced by more costly fuel

Thursday, 26 March 2026 16:54:22 (GMT+3) San Diego

US long steel prices were stable again this week, as reports of increased domestic supply availability and steady to potentially lower US Midwest scrap pricing for April are being offset by rising oil-related domestic and global transportation costs as a result of the continuing war in Iran, now in its fourth full week, market insiders told SteelOrbis.

Domestic fuel price increases are having an affect on the cost of domestic transportation, insiders told SteelOrbis, as the price of diesel fuel in the Chicago, Illinois, continued beyond $5.25 a gallon (March 25), up from about $5.06/gal one week earlier and up nearly 35 percent from on average $3.89/gal one month before.

“Trucking fees in the US are up between 20-30 percent since the price of diesel has spiked,” said one Midwest-based long steel insider. “I think higher trucking fees are going to have an impact on a wide range of industries, not only steel.”

And while transportation costs are reported on the rise, the price of domestic rebar on a Midwest FOB mill basis has yet to increase, most recently trading steady for a third week at $47.50-48.50/cwt., ($950-970/nt or $1,047-1,069/mt), market insiders told SteelOrbis. Insiders said current rebar and wire rod lead times are starting to improve as more production capacity becomes available from Nucor, Lexington, as well as Hybar Steel. Lead times quoted for new production have dipped to 4-6 weeks, they said, down from earlier reports at 6-8 weeks.

In the domestic wire rod markets, insiders told SteelOrbis pricing remains flat for a second week, though remains more subject to potential price increases, as supply is still reported tight as a result of reduced production from Peoria, Illinois-based Liberty Steel’s 700,000-ton wire and rod plant.

Average SteelOrbis spot prices for wire rod mesh on an ex-mill Midwest basis are reported steady at $49.00-50.00/cwt., ($980-1,000/nt or $1,080-1,102/mt), though up from $48.50-49.50/cwt., ($970-990/nt or $1,069-1,091/mt) reported three weeks earlier.

US import long steel prices flat on supply bump, energy/freight pricing slip

Friday, 27 March 2026 16:42:53 (GMT+3) San Diego

Import long steel prices were reported stable this week, following a steady to higher assessment one week prior, amid reports of slightly improved supply, even as energy pricing and freight rates are retreating from recent highs, as the ongoing war continues in the Middle East, market insiders told SteelOrbis.

On the US Gulf Coast, import rebar on a loaded truck basis remains flat for a fourth week following an earlier $0.50/cwt., price rise to $44.50-45.50/cwt.,($890-910/nt or $981-1,003/mt). US East Coast import rebar pricing also was assessed stable to week-ago levels at $45.00-46/cwt., ($900-920/nt or $992-1,014/mt).

Following this past week’s reports of fewer suppliers on offer as a result of rising fuel surcharges, import pricing for wire rod mesh on a DDP loaded truck basis Houston, Texas, was reported flat this week at $46.50-47.50/cwt., ($930-950/nt or $1,025-1,047/mt), though up from $46.00-47.00/nt ($920-940/nt or $1,025-1,047/mt) reported following SteelOrbis surveys two weeks earlier.

“On the import side, some Korean rebar shipments during February and March have filled recent holes which had caused US Gulf Coast and East Coast mills to be short supply,” the US Gulf Coast long steel importer told SteelOrbis. “Prices could drop, but it’s probably a temporary drop we’re looking at.”

Media reports indicate this week that Iran allowed a “gift transit” of 10 oil tankers to flow through the contested Strait of Hormuz, though shippers were limited to those not linked to the US or Israel. While hostilities continue and the US considers the use of elite ground troops after a recent 10-day extension by US President Trump, Iran continues its “selective transit model,” allowing only non-hostile vessels to transit the Strait.

And, while fuel costs remain only one component in total shipping fees, the price of benchmark Brent crude oil remains about 40-50 percent higher than when the Iran conflict started on Feb. 28. More importantly, according to shipping industry monitor Ship and Bunker, the average price of very low sulfur fuel oil (VLSFO) used by many ships across the world’s 20 largest refueling ports, has declined to about $943.50/mt (Mar 26), off from a high of about$1,068/mt (Mar. 20), though still considerably higher than $544/mt reported a day before hostilities began with Iran.

“It remains hard to predict what the world will do in reaction to the ongoing conflict in the Mideast,” said one US Gulf Coast long steel importer, when asked about his outlook for future import long steel pricing.

US April scrap maintains sideways to down sentiment, East Coast export markets could be key

Friday, 27 March 2026 09:50:37 (GMT+3) San Diego

Echoing a market call that began nearly a month ago, the outlook for April scrap remains locked at sideways to lower, though insiders caution the extent of likely price declines next month for US Midwest pricing could depend on how much scrap gets exported during the fast-approaching supply negotiations.

“I think people have largely thrown in the towel for April and conceded that prime scrap will trade sideways, while cut grades could move $10-20/gt lower,” said one US Midwest-based scrap broker. “On the US East Coast, I would keep an eye on export scrap, as some buyers may emerge in trade.”

Even as rising diesel fuel costs for delivered scrap in the US continue because of climbing oil prices, mills surveyed remain convinced April pricing will be down. “April scrap markets are still set to move down,” said one US Midwest-based mill scrap buyer. “I’ve heard down $20/gt from the mill perspective,” said still another US Gulf Coast-based scrap trader. “It mostly looks sideways,” remarked a final US Gulf Coast scrap insider to SteelOrbis.

Based on a sideways to down expectation for April scrap, US Midwest local busheling and shredded scrap grades could settle on a delivered to mill basis at or below $445-455/gt ($452-462/mt), and $445-450/gt ($452-457/mt), respectively. P&S and HMS scrap might settle on a delivered to mill basis $10-20/gt less at $406-416/gt ($412-423/mt) and $370-390/gt ($376-396/mt), respectively.

As the SteelOrbis Weekly Scrap Report went to press (March 26), the price of benchmark spot Brent crude oil stood at about $107 a barrel (/bbl), off slightly from one week prior when prices spiked to over $110 per barrel (/bbl) following tit-for-tat missile and drone attacks on Middle East energy infrastructure assets by both Iran and Israel.

Do you have any questions? Check out our FAQ!Check out the most frequently asked questions about the service and products of StaalX. We are always here to chat with you in the chat boxes from the site or on the support telephone number below.

Contact us websupport@staalx.com or +1 (708) 697-3227

Follow StaalX on

|

-article_image.jpg&w=1920&q=75)

.jpeg)