Updates From This Week

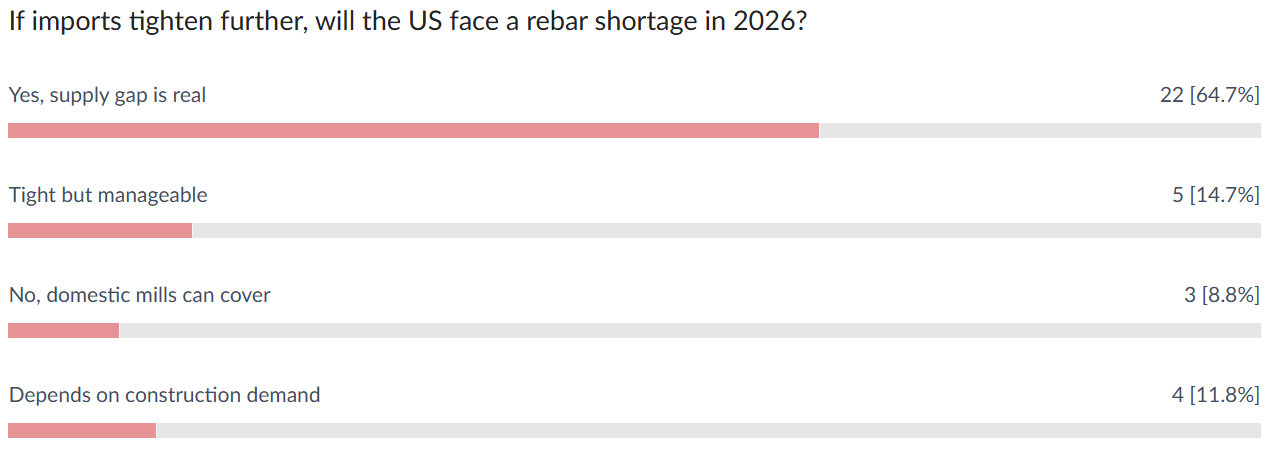

With massive trade barriers already squeezing imports of wire rod and rebar, global supply options were already meager. The conflict in Iran has now introduced a new layer of volatility to the supply chain. The most immediate implications are rising ocean freight rates driven by higher bunker costs and surging insurance premiums. For volume shipments, added costs have reached $10 to $20/mt so far. As the conflict drags into its third week, rates could climb further as "War Risk" surcharges become standardized. Many foreign producers have shifted into a wait-and-see mode; while long-distance trade is handicapped by these risks, local and near-shore trade is expected to increase. This shift will likely keep traditional North African and Asian suppliers focused on their domestic markets. Prior to the strikes in Iran, Asian mills—particularly in Vietnam (wire rod) and South Korea (rebar)—were aggressive. However, these producers are now pivoting away from the US market as their home-market margins improve. In Vietnam, the dominant mill recently raised prices, citing a surge in domestic orders. With few import options left for wire rod, offer prices have climbed, though they remain marginally more competitive than domestic levels. Domestic Supply Dynamics The US domestic wire rod supply remains tight. While there is no acute shortage, there is zero "slack" in the system. The wire-drawing business continues to hum along with robust demand, leaving buyers concerned about their ability to secure additional tonnage. Mills are signaling that another domestic price increase may be imminent, even as scrap prices stabilize with the improving weather. In the rebar sector, US mills have finally caught up. Hybar and Nucor’s Lexington micro-mill are now supplying meaningful tonnage to the market. Recent import arrivals have also helped alleviate spot shortages of specific sizes and grades, causing "spot" prices in the Texas market to retreat slightly. Conversely, Mexican supply has virtually exited the US rebar market following the 2025 tariff hikes and high antidumping rates. For remaining rebar imports, offers will almost certainly rise, even if domestic prices hold steady for now. Outlook Overall, buyers remain wary of price levels reminiscent of the record highs seen at the start of the Ukraine-Russia conflict. While markets typically adjust to high prices through demand destruction, the ongoing AI infrastructure boom—which requires massive amounts of structural steel for data centers—may sustain US construction activity for several years. However, with the Iran conflict showing no signs of de-escalation, we may only be at the beginning of a deepening global crisis. Weekly Poll Which factor will impact the US wire rod & rebar market the most in the coming weeks? Last Week's Poll Result  🚀 Coming Soon: StaalXneXtThe steel market is evolving. So are we. StaalXneXt is the next phase of the StaalX platform — built to expand access, increase supply visibility, and create smarter connections between buyers and sellers across long products and beyond. Designed for greater transparency and deeper market reach, StaalXneXt will introduce a more dynamic multi-vendor environment — while maintaining the reliability and performance our partners expect. Launching soon. Stay tuned — the next evolution of steel commerce is almost here.  Explore the upgrades at www.staalx.com or get in touch today with websupport@staalx.com to see the difference.  🎧 Missed Episode 19? Catch up now — we break down how the escalating Iran conflict could impact U.S. construction costs, steel pricing, and global supply chains in 2026. From rising oil and freight costs to disruptions around the Strait of Hormuz, the episode explores what contractors, distributors, and steel buyers should watch in the months ahead. Listen now on ▶️ YouTube | 🎵 Spotify | 🎙 Apple Podcasts 👉 Follow the StaalX Construction & Steel Podcast for weekly insights on market shifts, freight trends, and sourcing strategies.  From our content partner, SteelOrbis .jpeg) US domestic long steel prices steady with flat March scrap settles, growing supply Thursday, 12 March 2026 22:07:48 (GMT+3) San Diego US domestic rebar and wire rod prices were steady this week, continuing a trend reported a week earlier, following March’s flat scrap price settlements and amid continued reports that domestic long steel production, primarily in the form of rebar, continues to increase, market insiders told SteelOrbis. Insiders said increasing long steel output from Charlotte, North Carolina-based Nucor’s 430,000-ton per year Lexington rebar mini mill, as well as boosted output from Hybar Steel's 700,000 per year plant in Arkansas is keeping a lid on domestic rebar price increases. “At the moment, new mills in the US continue to pump out more tons of rebar into the market which is keeping prices pretty flat,” said one Midwest rebar insider. “We’re also hearing more reports of an expectation for lower scrap prices for April.” During the recent March buy-cycle ferrous scrap negotiations, March US Midwest shredded scrap, most often quoted as a key input for domestic rebar production, traded steady to February price levels at $445-450/gt ($452-456/mt). Since the beginning of 2026, SteelOrbis data shows Midwest shredded scrap pricing has increased more than 7 percent, while rebar pricing has gained about 3.2 percent. Prior to recent flat scrap settles, US scrap prices finished higher for each month since December. April scrap is seen steady to potentially $10-20/gt less, scrap insiders told SteelOrbis. Importers said the ongoing conflict with Iran could cause long steel import prices to continue higher, which might make domestic supply an even more attractive supply option. And while import rebar pricing posted steady this week, import wire rod prices posted increases amid reports that some overseas mills were not offering new supply as Midwest tensions continue and soaring oil prices boosted the price of shipping product to markets. Domestic rebar prices on an FOB Midwest mill basis remained flat on the week at $47.50-48.50/cwt., ($950-970/nt or $1,047-1,069/mt), off from $48.00-49/cwt., ($960-980/nt or $1,058-1,080/mt) two weeks prior, a level where pricing stood unchanged for five weeks. In the wire rod markets, insiders said supply-side issues could continue to support domestic long steel prices near term, especially wire. And, despite some seasonal declines in domestic demand ahead of the start of the spring construction season, insiders continue to report output from Peoria, Illinois-based Liberty Steel remains below its stated 700,000 ton capacity. The late-January sudden closure of Alton Steel’s 750,000 ton electric arc furnace in Alton, Illinois, also could continue to fuel pricing strength for large-sized wire rods, they said. In the domestic wire rod markets, following a week-ago $0.50/cwt., price increase, prices finished flat at $49.00-50.00/cwt., ($980-1,000/nt or $1,080-1,102/mt), up from $48.50-49.50/cwt., ($970-990/nt or $1,069-1,091/mt) two weeks earlier. Insiders told SteelOrbis this week they expect wire rod pricing to remain strong near term with additional weekly price increases likely as domestic supply could remain tight with imports limited, especially as tensions remain heightened in the Mideast. US import long steel prices steady to up as Iran war boosts shipping fees, less mills offer Thursday, 12 March 2026 20:04:17 (GMT+3) San Diego US import rebar and wire rod pricing was reported steady to higher for now a second week, following the Feb. 28 start of the US-Israel-Iran war, market insiders told SteelOrbis. A combination of higher shipping and energy costs with reduced long steel availability as some overseas mills refrain from offering while war-related risk premiums remain heightened, is likely to continue to be supportive for prices, they said. “I would say the Iran war has significantly raised freight rates and caused some overseas mills to refrain from offering,” reported one Midwest-based long steel insider. “As a result, those mills that are still in the market have raised their prices.” He continued, “In addition, domestic pricing is now at the highest levels seen since Russia invaded Ukraine in February 2022.” On the US Gulf Coast, import rebar on a loaded truck basis was reported flat for a second week following an earlier $0.50/cwt., rise at $44.50-45.50/cwt.,($890-910/nt or $981-1,003/mt). US East Coast import rebar pricing also was assessed steady to week-ago levels at $45.00-46/cwt., ($900-920/nt or $992-1,014/mt). And while higher import rebar pricing has yet to manifest as US long steel producers continue to ramp up productive output, importers said wire rod import pricing has begun to rise because US supply remains more limited with production from several key mills, among them Liberty steel and Anton Steel reduced or eliminated. “On the US rebar side, several new US mills (Nucor North Carolina and Hybar) continue to pump tons into the market and that’s keeping import and domestic prices stable,” the Midwest steel insider added. In the import wire rod markets, insiders said reduced offers from overseas producers caused prices to increase on average $1.50/nt to $46.00-47/cwt.,($920-940/nt or $1,014-1,036/mt), on a DDP loaded truck basis, up from $44.50-45.50 ($890-910/nt or 981-1003/mt) one week earlier. About 20 percent of the world’s total oil supply, or about 20 million barrels of oil daily are transported through the Strait of Hormuz, which borders the country of Iran. And, despite news that significant oil supplies would be released from strategic reserves, Brent crude oil prices currently remain nearly 37 percent higher than since the conflict started, trading at over $100/ barrel, the highest level since June 2022. Higher crude prices, insiders added, will mean higher prices for ship bunker fuel, making it more costly to ship steel and other commodities to markets. April US scrap seen steady to down amid stable March settles, better yard inflows, lower exports Thursday, 12 March 2026 23:21:01 (GMT+3) San Diego The price of April US ferrous scrap is heard sideways to down next month as a result of increased supply tied to better weather-related scrap inflows into local collection yards, market insiders told SteelOrbis. Insiders added that sharp increases in freight rates on export vessels headed to overseas scrap markets could lead to increased US supply as export scrap backs up at US ports. “We’re hearing that April scrap is very much flat to down” said one US Midwest mill-based scrap buyer. “Domestically, April pricing is looking sideways,” said another Midwest scrap insider. “On the export side though, scrap destined for Asian markets is up about $30/gt because of increased shipping rates.” “We expect a bit lesser price of down $10-20/gt for obsolete grades (HMS,P&S),” noted still another Midwest scrap insider. “I would not be surprised to see primes settle sideways for April.” Based on a sideways to lower expectation for April scrap, US Midwest local busheling and shredded scrap grades could settle on a delivered to mill basis at or below $445-455/gt ($452-462/mt), and $445-450/gt ($452-457/mt), respectively. P&S and HMS scrap might settle on a delivered to mill basis $10-20/gt less at $406-416/gt ($412-423/mt) and $370-390/gt ($376-396/mt), respectively. Do you have any questions? Check out our FAQ!Check out the most frequently asked questions about the service and products of StaalX. We are always here to chat with you in the chat boxes from the site or on the support telephone number below. Contact us websupport@staalx.com or +1 (708) 697-3227 Follow StaalX on |

March 16, 2026 at 2:40 PM

Share

Import Long Products Market Rocked by Iran Conflict and Limited Supply Options

This article is available to StaalX members. Please log in or sign up to read the full article.