-article_image.jpg&w=1920&q=75)

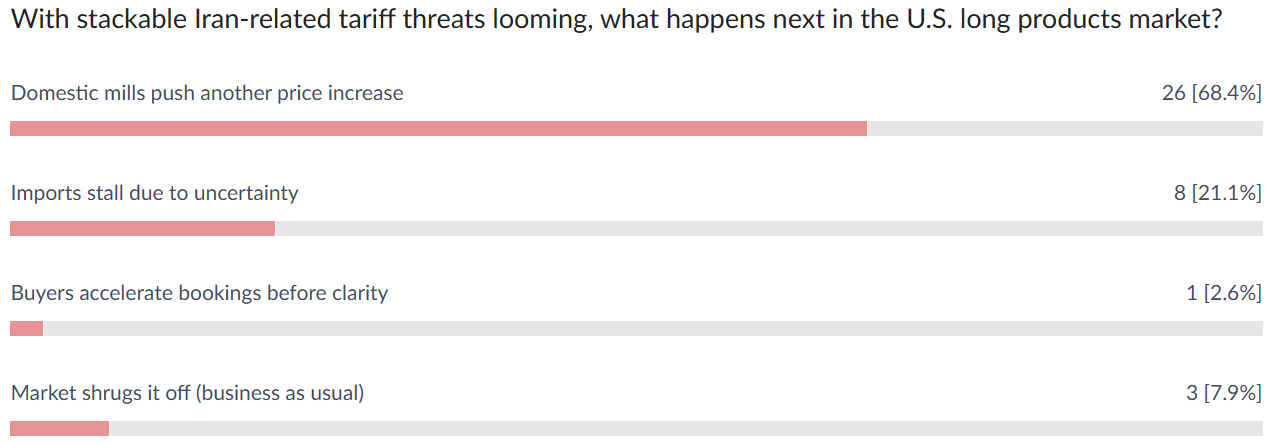

Updates From This Week

The upward momentum for long products continues, underscored by last week’s $30/ton increase for wire rods and a significant $60/ton jump for structural beams. These two categories remain in high demand, insulated by limited domestic production and a lack of meaningful import competition. While domestic wire rod mills are operational, various production "hiccups" and seasonal maintenance have kept capacity utilization rates suppressed. With imports remaining "few and far between," any unexpected mill outage could trigger a critical supply squeeze; current lead times for new import orders are already pushing into July. Conversely, the rebar market is beginning to feel the weight of new domestic capacity. The ramp-up of Hybar and Nucor’s Lexington micro-mill has introduced fresh volume into the market, as both players aggressively vie for domestic share. While scheduled maintenance outages at several CMC mills will temporarily remove some tonnage from the market, the combination of increased domestic supply and the arrival of Korean and Turkish shipments is finally easing the "extreme shortage" seen last quarter. This shift has forced domestic rebar sales reps—who had grown accustomed to a "sleepy" seller's market—back to the phones to secure orders. Despite this local volatility, broader construction and demand fundamentals remain robust. Infrastructure projects and data center builds continue to provide a solid floor for consumption. We do not anticipate a rapid reversal of these tight market conditions; while large-volume buyers may snag the occasional "spot deal," overall pricing is expected to remain elevated through at least the second half of the year. Weekly Poll Will new domestic capacity push rebar prices lower this quarter? Last Week's Poll Result  🚀 Coming Soon: StaalXneXtThe steel market is evolving. So are we. StaalXneXt is the next phase of the StaalX platform — built to expand access, increase supply visibility, and create smarter connections between buyers and sellers across long products and beyond. Designed for greater transparency and deeper market reach, StaalXneXt will introduce a more dynamic multi-vendor environment — while maintaining the reliability and performance our partners expect. Launching soon. Stay tuned — the next evolution of steel commerce is almost here.  Explore the upgrades at www.staalx.com or get in touch today with websupport@staalx.com to see the difference.  🎧 Missed Episode 17? Catch up now — we examine the growing paradox in the U.S. construction market: backlogs have dropped to a four-year low, yet contractor confidence remains surprisingly strong. From shifting capital flows into heavy physical assets and Alphabet’s historic $32B AI infrastructure bond sale to steel price hikes, tariff pressures, and evolving demand dynamics, this episode unpacks what’s really driving sentiment — and whether optimism is justified as we move deeper into 2026. Listen now on ▶️ YouTube | 🎵 Spotify | 🎙 Apple Podcasts 👉 Follow the StaalX Construction & Steel Podcast for weekly insights on market shifts, freight trends, and sourcing strategies.  From our content partner, SteelOrbis .jpeg) US domestic long steel prices steady as scrap settles higher; mill price increase may wait Friday, 13 February 2026 00:51:10 (GMT+3) San Diego US domestic rebar and wire rod prices remaind flat this week, even as pricing for February scrap posted gains for now a third straight month, market insiders told SteelOrbis. And while continued increases in scrap prices will certainly raise US mills’ steel production costs, not all are convinced further price increases from US mills are forthcoming, at least not right away. Additional mill price increases, they contend, could encourage the entry of an increased amount of long steel imports, prompting US mills to give back key market share gained after 50 percent steel tariffs reduced imports to a trickle earlier this year. Reports continued this week that long steel supply currently is in transit from South Korea and is expected to arrive in the US during March and April. At press time, initial data from the Washington, D.C.-based International Trade Administration’s (ITA) US Steel Import Monitor, finds rebar import licensing requests totaled 62,618 mt for February, down nearly 25 percent compared with a 83,243 mt total in January and 103,281 mt in February of last year. Year on year, licensing data requests are off by 19.4 percent. In the weekly rebar spot markets, domestic supply on an FOB mill basis was assessed with most transactions noted at $48.00-49.00/cwt, ($960-980/nt or $1,058-1,080/mt), on average $48.50/cwt, ($970/nt or $1,069/mt), unchanged from a week earlier. “Prices already have increased a lot. Some people are skeptical that price increases will continue because of a general pessimism about the economy,” said a long steel insider. Following the winter storm three weeks ago, many US states have returned to more moderate temperatures, but the Midwest and Northeast remain cold, causing continued slow shipments of steel scrap. “Scrap is up, but there is a lot of hesitation in the market as far as a new potential [price] increases,” said a SteelOrbis insider, “I have also heard there is a lot of import rebar coming in.” US prime busheling Midwest scrap for February delivery was up $30/gt this week, settling at $445-455/gt ($451-461/mt). Midwest shredded scrap gained $30/gt to $445-450/gt ($452-456/mt), while cut grades, like P&S and HMS, settled $20/gt higher at $421-431/gt ($427-437/mt) and $385-405/gt ($390-410/mt). In the domestic wire rod market, domestic supply on an FOB mill basis was assessed with most transactions reported steady at $48.00-49.00/cwt ($960-980/nt or $1,058-1,080/mt), or an average of $48.50/cwt ($970/nt or $1,069/mt), unchanged from seven days ago. “Liberty is not producing as much, and not keeping their promises,” remarked a long steel insider. Continued outreach by SteelOrbis to media officials at the 700,000 ton per year Liberty facility remained unsuccessful at press time. According to a recent Associated Builders and Contractors survey, “US construction backlog fell to 8 months in January, down 0.2 months from December and now sits at its lowest level in four years”. On the domestic long steel demand side, insiders reported an improving US construction industry sentiment as infrastructure and data center projects “regain traction.” US import long steel pricing steady, domestic price pressures on the rise with higher scrap Thursday, 19 February 2026 17:56:44 (GMT+3) San Diego US import rebar and wire rod prices were steady this week although they could be poised for an increase soon as reports continue of increased import demand as high US scrap prices continue to contribute to upward movement in US steel markets, making further room for imports, market insiders told SteelOrbis. Following recent $20-30/gt higher settlements in US scrap markets, on February 12, steel makers Gerdau and Steel Dynamics Inc., announced a price increase of $40-60/ton on their posted prices for wide flange beams, standard beams, misc. beams, piling, and select angles and channels. That same day, Charlotte, North Carolina-based steelmaker Nucor announced another $30/ton ($1.50/cwt.) increase in its domestic wire rod pricing, with a later structural price increase sent to customers on Feb. 17. In both December and January, Nucor announced price increases for its rebar products. To date, no further rebar increase announcements have been forthcoming from Nucor. And, while it remains unclear how soon and if, price increases across US wire rod markets will be accepted by the marketplace, insiders said the structural steel price increase are more likely to be accepted by the markets right away as a result of lower inventory levels. “Raw material cost inflation (scrap) is now flowing through to finished steel pricing across structurals and rod,” said one Houston-based rebar importer. “Recent mill announcements and scrap settlements confirm that the North American long steel market is shifting from stable, to firm with upward momentum, heading into the spring construction season.” During February scrap trade, shredded scrap in the US Ohio Valley increased $30/gt to $445-450/gt ($452-456/mt), while prime busheling scrap sold $30/gt higher at $445-455/gt ($451-461/mt). Since the new year, shredded scrap prices have risen more than 19 percent, while Midwest busheling scrap prices have increased a more modest 12.5 percent, SteelOrbis data shows. “Wire rod could potentially trade $1.50/cwt., higher by the beginning of the (new) month,” said one Chicago-based steel insider. “But, on the structurals, the markets are most likely to accept the price increases now because supply remains fairly tight on beams.” “Rod markets already were tight in select diameters,” added one US East Coast rebar insider in reaction to questions about recent mill price increases. “Scrap strength and improved order entry has allowed mills to push through recent price increases faster.” On the US Gulf Coast, import rebar on a loaded truck basis is reported steady from week-ago levels at $44.00-45/cwt, following earlier declines. Insiders said delivery to US East Coast ports will add an additional $20/ton to $45.00-46/cwt., ($900-920/nt or $992-1,014/mt), also steady once again on the week. Import insiders said South Korean producers may seek higher pricing following the New Years holiday, which began with the new moon on Feb. 17 and continues through the Lantern Festival on Monday, March 3. For the moment, imported wire rod mesh on a DDP loaded truck US Gulf basis, is discussed steady on the week at $43.50-44.50/cwt., ($870-890/nt or $959-981/mt), though a price increase is likely soon. “On the import side, all of the product currently coming into the US is South Korean,” said one US-based market insider. “More imports are available right now on the Gulf Coast, and we’re starting to see the imports reflected in the statistics. According to data from the US Dept. of Commerce’s International Trade Administration (ITA), Steel Import Monitor, total rebar imports from South Korea into the US were 23,800 metric tons in November 2025, up from 12,000 mt of actual imports reported one year prior. And while ITA’s rebar import license data is not always a one for one to actual imports reported, preliminary data for February 2026 shows a total of 57,300 mt of imports for the month, a nearly five-fold increase from the 12,200 mt of actual imports reported to ITA for all of February 2025. Some insiders told SteelOrbis recently further US scrap-inspired price increases might not occur soon or might be more limited from US domestic mills, especially since additional upward movement in domestic pricing could further encourage the entry of additional imports over the next several months, crimping recent hard-earned growth to domestic steel mill market share, they said. “Some importers are increasingly worried about ongoing levels of US demand,” added the Midwest-based long steel insider to SteelOrbis. “Given continued lackluster demand from the US construction sector, some are concerned that there may soon be too much supply chasing limited market, especially once additional US productive capacity comes on line later this year.” He continued. “I tend to be more optimistic than many, and don’t see much downside in the US market over the next six months as the US economy continues to grow despite claims by many that inflation would increase and stunt growth.” Despite still mixed feelings about the effects of tariffs on longer-term US growth, data suggests steel demand could remain limited nearer term. According to a recent report from the Dodge Construction Network, the Dodge Momentum Index (DMI) -which measures US construction activity and planning- declined 6.3 percent in January to 272.7 (2000=100) from a downward-revised December reading of 291. Over the month, commercial planning fell 7.2 percent and institutional planning momentum slumped 4.4 percent, the report said. And while monthly numbers were down, year-over-year comparisons were more encouraging, with the DMI index up 29% when compared with January 2025 levels, while the commercial segment was up 26 percent -up 17 percent when data centers are removed- and the institutional segment increased 34 percent over the same period. “Planning momentum cooled in January across most commercial and institutional sectors,” said Associate Director of Forecasting at Dodge Construction Network, Sarah Martin. “Data center projects continue to lead the way, but after elevated activity in late 2025, most nonresidential sectors are now easing into a more sustainable growth pattern.” March US steel scrap seen mixed for now, February weather and inflows key to direction Friday, 13 February 2026 21:13:16 (GMT+3) San Diego This week’s exclusive SteelOrbis weekly survey of US scrap market participants finds a mixed call for the likely price direction for March scrap, with suppliers calling the market steady to potentially up depending on weather and February inflows, while mill scrap buyers see the market steady to potentially lower as expectations for warmer weather, they say, could improve the ongoing scant supply situation. At this early juncture in March scrap discussions, SteelOrbis calls the market most likely sideways, though subject to change depending on the perception of supply on hand at mills and suppliers as buy-cycle negotiations commence in early March. Following on February’s $20-30/gt scrap price increase for markets east of the US Mississippi River, suppliers told SteelOrbis inventory on hand still remains limited owing to reduced inflows as a result of recent extreme cold weather, which caused vehicle, transport and equipment issues across more than 30 states. Available scrap at mills, they say, may have been allowed to get too low and recent weather was not helpful in building inventory levels. “There’s been lots of talk in the markets about sideways scrap for March,” said one US Midwest scrap insider. “Inflows into supply yards remain slow, but they are reported to be improving a bit.” One Midwest scrap broker told SteelOrbis prime scrap, especially, could continue higher for March. “I think we may see primes tick up a bit, while cut grades (P&S and HMS) may remains flat.” Mill buyers, on the other hand, said warmer weather should improve scrap inflows. “I’d say sideways to down,” reported one Midwest mill scrap buyer. “Warmer weather will help us all.” “We see next month flat to lower, because of much better weather in March” reported another US South scrap buyer. According to short-term forecasts from the US National Weather Service (NWS), temperatures across most of the Eastern US are expected to moderate from recent below-normal levels. A shift from extreme cold to a warmer trend, featuring active weather, including rain and snow showers is possible in the South and Mid-Atlantic states. NWS short-term forecasts for the Midwestern US calls for high winds as well as the potential for heavy snow across the upper Midwest and Northern Plains. Based on a current conservative sideways call for March scrap, US Ohio Valley prime bushing scrap could settle near its $30/gt higher February settlement at $445-452/gt ($452-462/mt), while March shredded material could finish near its $30/gt higher February finish near $445-450/gt ($452-456/mt). In the cut grades, a sideways expectation for P&S scrap near $421-431/gt ($427-437/mt) is likely, following its $20/gt February gain. March HMS, which also rose $20/gt this month, was likely to settle near $385-405/gt ($390-410/mt), scrap insiders told SteelOrbis. In the US Northeast, a current sideways March expectation could yield busheling scrap near $400-420/gt, ($406-426/mt), following its $30/gt February gains. Shredded scrap, which also rose $30/gt, could finish near $395-405/gt ($400-410/mt), while P&S and HMS grades -which both saw $20/gt February price increases- could finish near $350-360/gt ($355-365/mt), and $365-380/gt ($370-385/mt), respectively. Do you have any questions? Check out our FAQ!Check out the most frequently asked questions about the service and products of StaalX. We are always here to chat with you in the chat boxes from the site or on the support telephone number below. Contact us websupport@staalx.com or +1 (708) 697-3227 Follow StaalX on |

Need steel? Get an instant quote & save $500 off your first order

Search rebar, wire rod, wire mesh and more on StaalX. Check availability and book reliable delivery nationwide.