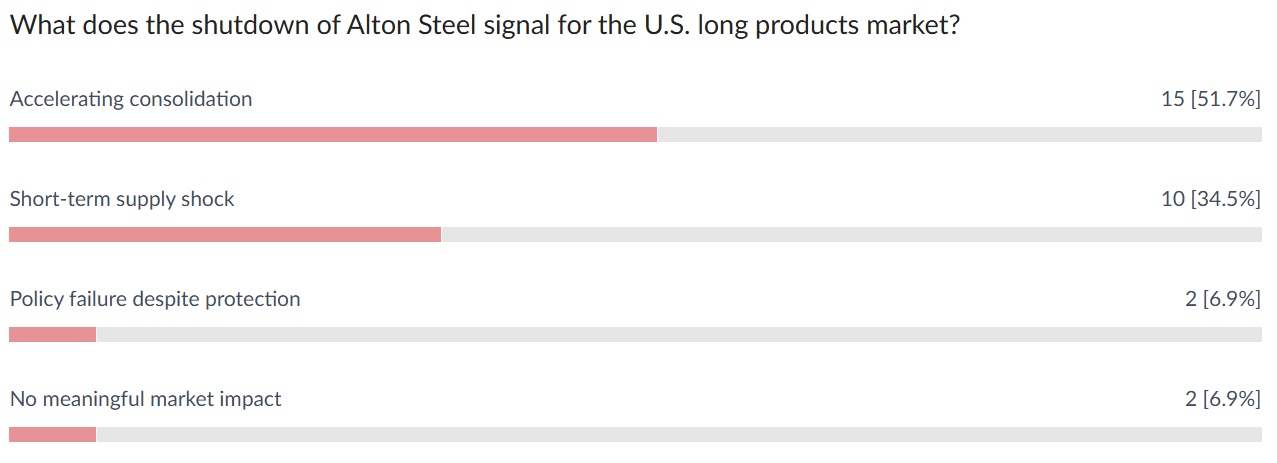

Updates From This Week It seems all the unpleasant tariff surprises arrive on Fridays via social media. This time, traders were jolted by the possibility of yet another tariff threat from President Trump. Several weeks ago, Trump threatened to slap 25% tariffs on countries doing business with Iran. He followed through by signing an executive order last Friday (Feb 6) to make it official, though the implementation remains somewhat opaque. While the new duties are threatened as ad valorem, the key takeaway is that they are stackable. Even though Section 232 tariffs are already at 50% for most origins, these potential Iran-related duties would be added to that existing burden, potentially pushing the combined total significantly higher—or, as the administration suggested, reaching a combined 25% floor for those not already heavily taxed. The Administration has yet to fully implement these measures. No doubt, Trump is waiting for the outcome of ongoing Iran negotiations. At the moment, he suggests talks are progressing well and hints at a "happy ending" that avoids military action or secondary tariffs against Iran's trading partners. But if negotiations break down, all bets are off; a massive military buildup could become the reality, and those tariffs will almost certainly be enforced. While the executive order doesn’t name specific nations, the primary trading partners impacted would likely be China, Turkiye, and the UAE. In the case of Turkiye, they remain a major exporter of rebar, structurals, and merchant bars to the U.S. These extra duties would not only hurt importers but likely halt Turkish volumes to the U.S. market entirely. Interestingly, Turkiye is not a major wire rod exporter to the States, so the impact on that specific niche should be minimal. While trade legislation threats come and go, the markets haven't lost their upward momentum. Scrap prices increased by $30 per ton in early February, a move that will undoubtedly keep the pricing trend for long products pointing up - even as some analysts worry the rally is running out of steam. We don’t get the impression that demand is "white-hot," but it is certainly adequate, fueled largely by AI infrastructure projects and data center builds. Meanwhile, domestic supply is strained; many customers are back on allocations as new mills struggle to reach full capacity and older facilities face operational "sputters." The window for import opportunities has been open for a few months now, and we are starting to see the physical results. Import statistics for early February already show arrivals of South Korean rebar and Vietnamese wire rod, with more shipments expected to hit the docks over the next several months. Weekly Poll With stackable Iran-related tariff threats looming, what happens next in the U.S. long products market? Last Week's Poll Result  🎯 Buy Steel with StaalXStaalX is the digital marketplace built for modern steel procurement. From rebar and wire rod to welded wire mesh and merchant bars, we help contractors, fabricators, and distributors source full truckload quantities with speed and transparency. Why StaalX?

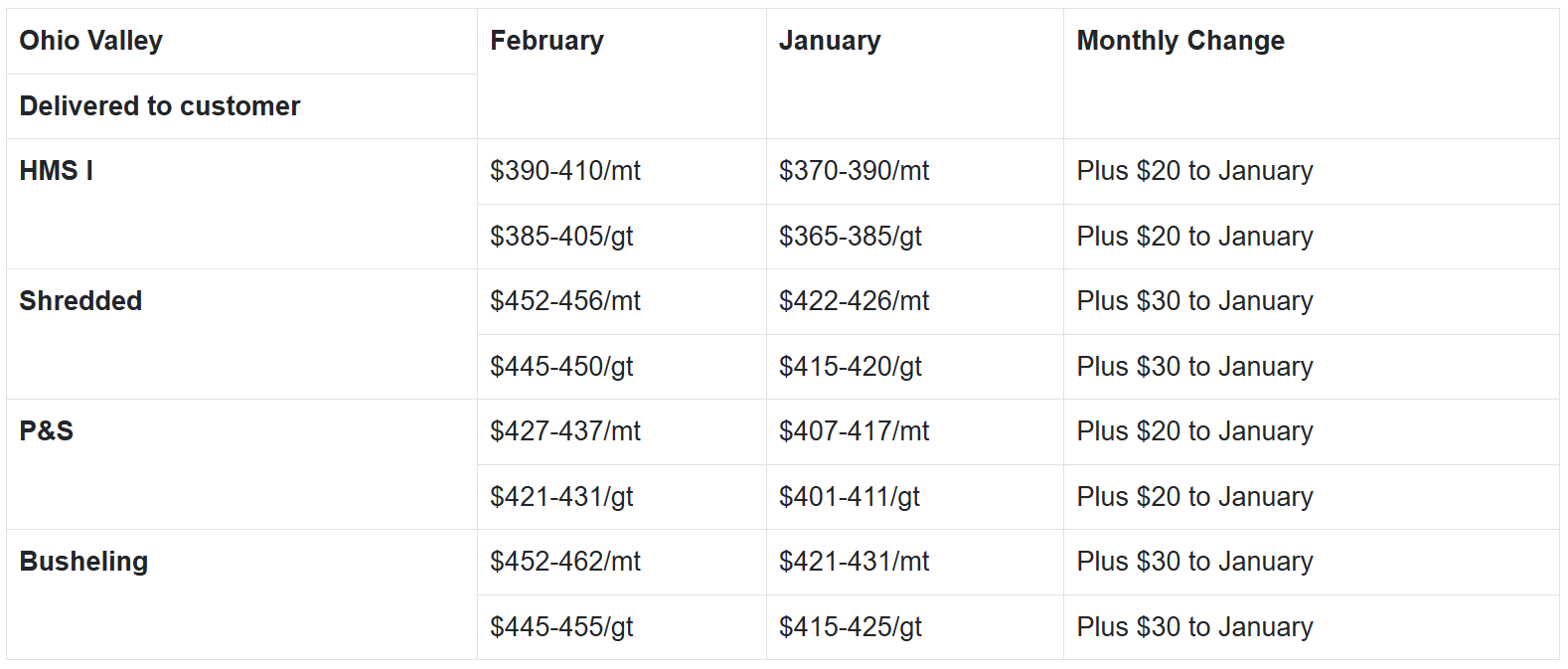

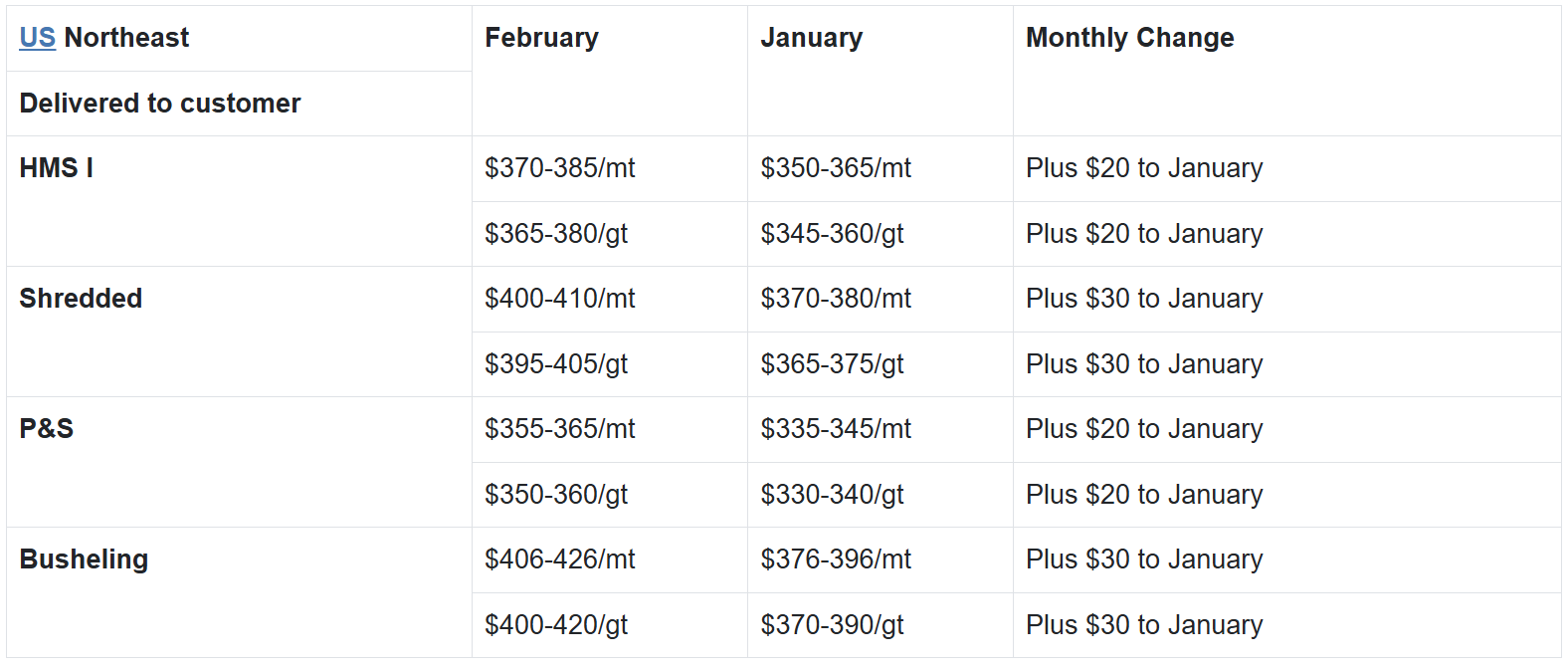

Stop chasing quotes. Start sourcing smarter.  Explore the upgrades at www.staalx.com or get in touch today with websupport@staalx.com to see the difference.  🎧 Missed Episode 16? Catch up now — we take a closer look at whether the long-standing Great Stagnation in the U.S. housing market is finally beginning to ease — or if recent improvements reflect short-term momentum rather than a true structural reset. From construction costs and steel supply volatility to tariffs, regulation, and policy reform, this episode explains what’s actually holding housing back — and what needs to change for a lasting fix as we head into 2026. Listen now on ▶️ YouTube | 🎵 Spotify | 🎙 Apple Podcasts 👉 Follow the StaalX Construction & Steel Podcast for weekly insights on market shifts, freight trends, and sourcing strategies.  From our content partner, SteelOrbis .jpeg) US long steel prices steady, rising scrap may prompt more price increases Thursday, 05 February 2026 20:05:32 (GMT+3) San Diego US domestic rebar and wire rod prices remained flat for a fourth straight week, though insiders told SteelOrbis early monthly domestic scrap trade could provide the impetus for further price increases from US mills soon. Insiders said recent increases in long steel prices have largely been the result of higher steel production costs, driven by the continued strength in local scrap values, even as rebar and wire rod imports remain slashed as a result of 50 percent steel tariffs. Cold weather across much of the US also was expected to delay or reduce scrap delivery to mills this month. “Scrap is a big driver right now and may pull long product pricing higher because the market remains relatively tight,” remarked one US Midwest-based market insider. In the weekly rebar spot markets, domestic supply on an FOB mill basis was assessed with most transactions noted at $48.00-49.00/cwt, ($960-980/nt or $1,058-1,080/mt), on average $48.50/cwt, ($970/nt or $1,069/mt), unchanged from a week earlier. Following winter storms two weeks ago that were estimated to have affected more than 200 million Americans across more than 30 states, extreme cold is forecast to continue in major market centers in the US Midwest and Northeast regions over the next several days, before moderating to more normal temperatures. And while weather was expected to moderate, recent record cold has caused key portions of the Ohio River to freeze over, reducing and delaying barge deliveries of steel scrap and other steel production components by as much as three days. Lake Erie, a major transportation route for steel making materials, was expected to freeze over fully this weekend, the first time in recent recorded history. Insiders added that the increased use of available trucking resources for the delivery of road salt also was expected to affect regional scrap delivery. “The rates that salt customers are paying for delivery has been awesome for our trucks,” remarked one US Midwest scrap supplier. “They have been much better than scrap, which was never the case.” At last report, US ferrous scrap for February delivery trades at $30/gt premiums across all scrap grades, meaning benchmark US Midwest shredded scrap used in rebar production might settle at $445-450/gt ($452-457/mt) later this week or early next. In the southern US, insiders told SteelOrbis mills are working hard to meet customer demand for long steel, though weather continues to remain problematic. Arkansas-based Hybar Steel is still producing despite the winter weather delays and stays the “primary swing [rebar] supplier,” according to one long steel insider. In the domestic wire rod market, domestic supply on an FOB mill basis was assessed with most transactions reported steady at $48.00-49.00/cwt ($960-980/nt or $1,058-1,080/mt), or an average of $48.50/cwt ($970/nt or $1,069/mt). “Liberty Steel is not producing well,” said one Midwest insider to SteelOrbis. “ It is getting uncomfortable for the wire rod guys. They are sputtering and looking outside for imports.” Continued outreach by SteelOrbis to media officials at Liberty Steel remained unsuccessful at press time. On the domestic long steel demand side, insiders report an improving industry sentiment for the depressed US construction industry, especially as the start of the spring construction season nears ahead of further cuts in interest rates, and ahead of approaching summer deadlines for government infrastructure funding requests under the $1.2 trillion Infrastructure Investment and Jobs Act. In other news, Illinois-based Alton Steel, a key domestic producer of steel rounds, round-cornered squares, and bar-in-coil, closed its doors this past week, according to a report from St. Louis Radio. Reports cited “aging infrastructure, intense market competition, and industry consolidation.” The closure will mean layoffs for more than 250 employees, including contractors and vendors. US import long steel steady to down; Asian imports and up US scrap could pressure Friday, 06 February 2026 02:16:18 (GMT+3) San Diego US import rebar and wire rod prices were steady to slightly down this week, following reports of limited declines a week earlier, as reports continued that a recent increase in long steel imports from South Korea might be staging to pressure prices further, market insiders told SteelOrbis. Rising US shredded scrap prices, they added, were also expected to increase the spread between import and domestic long steel prices, potentially making more room for imports to once again be competitive. “Long steel imports are all about South Korea right now,” remarked one US Midwest-based long steel importer. “We’re hearing reports that more steel may have arrived on the US Gulf Coast from Korea from the Pacific side through the Panama Canal in the $44.00-45/cwt. range ($880-900/nt or $970-992/mt).” One report of a potential South Korean rebar offer today (Feb. 5) at $42.00/cwt. was largely discounted as non-inclusive of on-shore stevedoring charges, currently estimated at $1.00-$3.00/cwt, insiders said. “Imports to the US are improving, but are not yet disruptive,” said another Gulf Coast-based long steel insider to SteelOrbis. “Import rebar prices remain largely steady, but the discount to domestic pricing has narrowed.” On the US Gulf Coast, import rebar on a loaded truck basis is reported a bit less on the week at $44.00-45/cwt, off $1.00/cwt or $20/nt from from recent SteelOrbis weekly estimates amid reports of improved inventory. Insiders said delivery to US East Coast ports will add an additional $20/ton to $45.00-46/cwt., ($900-920/nt or $992-1,014/mt), steady on the week. “Import pressure is increasing at the margin, but availability remains constrained by tariffs, duties, and long lead times,” the US Gulf Coast long steel importer added. In the US scrap markets, February US Midwest shredded scrap often used in EAF rebar production is trading at $30/gt premiums to earlier January settles at $445-450/gt ($452-457/mt), meaning US mills are facing further increases in steel production costs. Market insiders said rising scrap could mean another round of long steel price increases are forthcoming from US mills, further narrowing the price advantage between domestic and import long steel. In early January, Charlotte, North Carolina-based Nucor announced a $30/nt rebar price increase, following an earlier $30/nt increase during November. In the import wire rod markets, insiders said tightening domestic supplies could increase demand for shipments from Malaysia and Vietnam, though long lead times were a significant consideration. “Liberty Steel is not producing well,” said one US Midwest long steel importer. “It is getting a little uncomfortable for the wire rod guys. They are sputtering and looking outside for imports.” Weekly SteelOrbis average wire rod mesh import pricing on a DDP loaded truck basis remains stable for now at $43.50-44.50/cwt., ($870-890/nt or $959-981/mt). February US scrap settles $20-30/gt up on tight supply, weather and solid mill demand Tuesday, 10 February 2026 21:36:45 (GMT+3) San Diego US ferrous scrap prices during the recent February buy-cycle negotiations in the US Ohio Valley and US Northeast regions settled $20-30/gt higher than equivalent January values, based on reports of a continued paucity of supply at local yards, recent weather-related supply disruptions, as well as solid demand from US domestic mills during monthly supply negotiations, market insiders told SteelOrbis this week. US settled prices are below:   Do you have any questions? Check out our FAQ!Check out the most frequently asked questions about the service and products of StaalX. We are always here to chat with you in the chat boxes from the site or on the support telephone number below. Contact us websupport@staalx.com or +1 (708) 697-3227 Follow StaalX on |

Need steel? Get an instant quote & save $500 off your first order

Search rebar, wire rod, wire mesh and more on StaalX. Check availability and book reliable delivery nationwide.