| | | |

Are We Primed for a Q1 Pricing Rally?

|

|

If history is a guide, we know that the cold winter months typically bring collecting difficulties and supply-side constriction, often causing scrap prices to rise, sometimes in massive steps.

Conversely, the winter period, particularly the fourth quarter (Q4), is usually a soft spot for steel demand. Momentum doesn't traditionally pick up until February, driven by seasonal construction demand.

However, this year introduces a dynamic the steel market hasn't encountered before: the rush for data center construction. While virtually all other construction sectors are experiencing mediocre to weak activity, data center construction is pulling the entire industry forward with serious urgency.

Consequently, demand for long products is unlikely to see a slowdown in Q4, and this momentum will probably continue through the end of the first quarter (Q1) of 2026.

Flat-rolled products, the main volume drivers in steel markets, are just now starting to gain some pricing momentum. This segment is typically far more volatile, experiencing deeper valleys and higher peaks than the long products market. In other words, flat-rolled steel could be a whole lot more explosive if market conditions heat up.

The Impact of Rising Scrap and High Utilization

What would happen if scrap registers massive gains in December and January? Mills announced increases recently, even when scrap prices had been remarkably flat for the last six months. Why would they refrain from further price hikes, especially if rising scrap is also pushing costs upward?

After all, US rebar and rod mills are currently running near capacity. Therefore, it is not inconceivable that strong price increases for rebars and wire rods could be in the cards over the next several months.

The Looming Question of New Supply

But there is a significant counter-force: what if the new greenfield rebar mills ramp up quickly?

While currently in production, new facilities like Nucor Lexington and Hybar are yet to make a serious dent in the existing supply tightness. However, this situation could change rapidly, potentially capping future price increases.

Key Takeaway

The market is currently being pulled in two directions: strong, non-seasonal demand from data centers and the potential for a scrap-driven cost push vs. the imminent threat of new rebar capacity coming fully online. The balance between these forces will define Q1 2026.

|

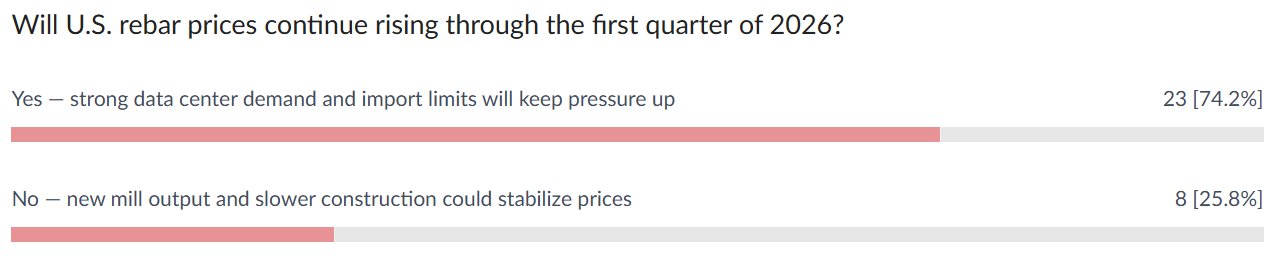

| | | Will the long-products market stay strong through winter despite seasonal slowdown? |

| | | | | |

🎙️ Missed Episode 9? Don't fall behind — we unpack how booming data-center construction is masking weakness in the wider construction market and what it means for the U.S. housing crisis.

From financing and labor being pulled into massive AI-driven data projects to chronic underbuilding of homes, Episode 9 explores why housing supply is stuck, how policy and permitting bottlenecks add pressure, and what needs to change so we can build both data centers and enough homes.

|

| | | | |

🏗️ StaalX Exhibits at World of Concrete 2026! |

|

Come see us at Booth #N3368 for a live demo of the digital steel marketplace that’s reshaping how the industry buys concrete reinforcements — including rebar, wire rod, welded mesh, and merchant bars.

🔥 Show-Only Bonus: - Claim your $500 discount code toward your first truckload order

- Enjoy gifts & giveaways for everyone who stops by our booth

No strings attached. Just our way of saying thanks for visiting.

|

| | | | From our content partner, SteelOrbis |

| | US domestic rebar prices up on domestic mill price increases, wire rod flat

Thursday, 13 November 2025 18:53:47 (GMT+3) San Diego |

|

US domestic rebar prices rose this week for the first time since early September after several domestic mills announced price increases effective Nov. 7 for bar products, market insiders told SteelOrbis this week.

Insiders said Nucor Bar Group announced a $30/nt ($33.07/mt) or $1.50/cwt., increase in its posted rebar pricing effective for new orders received before the close of business on Nov. 7. Nucor said all confirmed orders received by that date will be price protected if shipped by Nov. 21. Insiders said CMC followed suit with an equivalent increase of its own following the Nucor announcement.

And, while the mill didn’t specify a reason for the increase in its customer announcement, market insiders told SteelOrbis they have been expecting a price increase from the mills for several weeks now as a result of continued tight domestic supplies which is causing ongoing customer allocations, as long steel imports continue to be constrained by ongoing 50 percent Section 232 steel import tariffs.

“The domestic price of rebar is very close to the import price right now,” remarked one Midwest long steel importer. “Usually, the mill price is higher, and the import price is lower. This is an atypical situation,” he added. “This is bumping up rebar demand during the winter months, when demand is usually much lower.”

In the weekly rebar spot markets, domestic supply on an FOB mill basis was assessed with most transactions noted at $46.00-47.00/cwt, ($920-940/nt or $1,014-1,036/mt), on average $46.50/cwt, ($930/nt or $1,025/mt), up $1.50/cwt ($30/nt or $33/mt) from seven days earlier. While the rebar average rose a full $1.50/cwt., insiders report weekly trades ranged as low as $44.50 and as high as $48.00/cwt. ($890-960/nt or $981-1,058/mt), depending on the size of the customer.

“Everyone seems to be getting on board with the Nucor price increase,” noted one US East Coast rebar dealer. “On the wire rod front, we are expecting wire to follow the rebar pricing pretty closely.”

In the domestic wire rod market, domestic supply on an FOB mill basis was assessed with most transactions steady for now at $46.50-47.50/cwt ($930-950/nt or $1,025-1,047/mt), or an average of $47.00/cwt ($940/nt or $1,036/mt), unchanged from seven days ago.

“Not every product is as strong as rebar right now,” the Midwest long steel insider added.

On the raw materials front, although it remains early to make a fully informed determination for the local scrap market's’ December trend, most market sources told SteelOrbis they expect a sideways movement while a few mentioned a potential $10-20/gt increase for Detroit-area shredded material might be possible.

“I’m calling the December scrap market sideways right now,” said one US Midwest mill-based scrap buyer. “Though, it’s an easy call right now, because its very early.”

|

| US import long steel pricing steady as domestic markets begin upward price creep

Thursday, 13 November 2025 22:46:00 (GMT+3) San Diego |

|

US import long steel pricing remained stable this week, even as the first price increases from domestic mills since early September have caused domestic rebar prices to inch higher. Insiders told SteelOrbis if domestic pricing continues to advance, it could make imports a more attractive alternative to scant domestic supplies as supply allocations continue from mills, though time will tell, they said.

Insiders added that recent actions by the US Supreme Court to restrict US President Trump’s authority to use 50 percent Section 232 steel tariffs to limit the movement of cheap imports into the US, could cause imports activity to surge. A decision is expected by late-June 2026, according to media reports.

“Right now, supply and demand [in the US] are about even,” remarked an East Coast importer to SteelOrbis “But, people hate being on [supply] allocation from the mills, and the mills are saying that that it isn’t going to go away.” He continued, “Since companies can’t operate without bar, and the mills are telling people that it isn’t going to get better, imports will increase for the spring, especially, since [import] pricing is now the same or slightly less than domestic pricing.”

On the US Gulf Coast, import rebar pricing on a loaded truck basis was reported steady to week-earlier levels at $44.00-46.00/cwt., ($880-920/nt or $970-1,014/mt), though still up from $44.00-45.50/cwt., ($880-910/nt or $970-1,003/mt) three weeks earlier amid reports of shrinking supply availability at Gulf Coast warehouses. On the US East Coast, import rebar on a loaded truck basis remains stable for a fifth week at $44.00-46.00/cwt., ($880-920/nt or $970-1,014/mt). Limited reports of import rebar sales at $47.00/cwt., were noted recently, though insiders said they remain limited.

In the US domestic rebar markets, pricing rose $1.50/cwt., to $46.00-47.00/cwt., ($920-940/nt or $1,014-1,036/mt), the first such increase since prices rose $1.00/cwt., during the week of Sept. 1. Long expected mill price increase announcements from Nucor and later, CMC, dominated market chatter this week.

“On the US East Coast, we’re seeing some limited import activity from Egypt and some Arab countries,” the steel importer said. “And while we’re currently not seeing (long steel) coming in from Turkey per se, the market could get interesting if the Supreme Court rules against Trump on tariffs this year.”

“If the High Court rules that Trump doesn’t have tariff authority over Congress, and we have to pay all the tariff proceeds back, imports will flood the market,” he said. “Hang on, because it’s going to be a wild ride.”

Media reports indicate President Trump said tariff proceeds thus far are substantial. “Trump claimed this week that if the tariffs are deemed illegal by the Court under the 1977 International Economic Power Act, the refund process could exceed $3 trillion,” he said. “The justices were given wrong numbers about the repayment costs,” Trump said in the reports.

At issue is whether Trump had the authority to sidestep Congress in enacting Section 232 steel tariffs, initially claiming the global fees were a necessary part of controlling immigration and stemming the flow of deadly fentanyl into the US, mainly from Mexico and Canada. The later use of reciprocal tariffs, Trump says, are necessary to address a “national emergency that has developed over the trade deficit.” And while reciprocal tariffs in many cases have been negotiated lower, steel tariffs remain in place at 50 percent levels, sharply reducing key imports of steel and steel products from the US’ key trade partners Mexico and Canada.

On the import wire rod front, US Gulf Coast import pricing for wire rod mesh on a DDP loaded truck basis remained steady for yet another week at $42.00-43.00/cwt., ($840-860/nt or $926-948/mt). Insiders told SteelOrbis they expect wire rod pricing to advance on par with rising rebar values, especially since new facilities in the US South and Southeast remain at less than full capacity as plants continue to ramp up production.

While action on tariffs will be heightened through mid-2026, the outlook for Q1 long steel pricing could be staged for a shorter-term increase. Short -term weather forecasts from the US National Weather Service indicate a developing La Nina weather pattern across the US could cause colder and wetter early-winter weather across much of the US Midwest and Northeast, where many key steel production and scrap processing facilities are located. The US South and Southeast regions are expected to see warmer and drier weather as well as drought as a result of La Nina, the NWS report says. Last year, winter storms and extreme cold temperatures throughout the Midwest and Southeast, complicated the transportation of steel and scrap, leading to higher local steel prices and delayed deliveries, as roads, rails, and rivers were closed because of snow and ice.

|

| December US scrap seen sideways in early talks, higher pricing possible on better mill buying

Friday, 14 November 2025 19:24:05 (GMT+3) San Diego |

|

December US scrap pricing is being called mostly sideways in early market discussions with scrap buyers this week, though some suppliers told SteelOrbis higher prices are a distinct possibility, given the fact that many mills will have completed their annual maintenance operations by the start of December supply negotiations and could be in the market for more material next month.

During September, October and November, most US mills perform scheduled annual maintenance, reducing their need for scrap while mills remain shuttered. During September, scrap prices settled sideways to August values, while October saw a $10-20/gt dip in pricing across all scrap grades and regions. Recent November settles showed scrap mostly sideways once again, though Midwest busheling moved lower, as workable trading ranges narrowed, amid reports of plentiful supply in local markets, scrap insiders told SteelOrbis. Other grades finished solid sideways across all grades and regions.

“Right now there’s not much talk of December scrap going on in the market,” said one Midwest scrap insider. “More than likely it will settle sideways.” Another Midwest scrap broker said, “There’s nothing new to report yet on December, so we see it sideways.” Still, another Midwest mill buyer said, “I’m calling it sideways now, but that call is too easy because it’s early.” A Detroit-based supplier suggested potentially higher pricing. “We see the December market possibly up $10-20/gt for Midwest shred.”

While higher prices are a possibility, based on a developing consensus for a sideways to November settlement, US Midwest prime busheling scrap -which settled on average $18/gt less during November negotiations- could finish for December in the US Ohio Valley near $385-395/gt ($391-401/mt) on a delivered to mill basis. Midwest shredded scrap, which is called flat to potentially $10-20/gt higher, is likely to finish for December at or above its November settlement at $365-370/gt ($371-376/mt), though a solid market call remains inconclusive as buyers and sellers remain far apart. Ohio Valley HMS grades which finished sideways for November, are likely to settle flat again near $315-335/gt ($320-340/mt), while P&S scrap, which settled flat this month, could settle near its November close at $351-361/gt ($357-367/mt), scrap insiders told SteelOrbis.

Again, while it remains early, in the US Northeast, December prime busheling grade material is expected to settle flat near $340-360/gt ($345-365/mt), following its November sideways settlement, while shredded grades are now seen sideways to November near $315-325/gt ($320-330/mt). P&S and HMS grades could finish flat to the sideways November settles near $280-290/gt ($285-295/mt), and $295-310/gt ($300-315/mt), respectively, scrap insiders told SteelOrbis.

|

| |

Do you have any questions? Check out our FAQ! |

| Check out the most frequently asked questions about the service and products of StaalX. We are always here to chat with you in the chat boxes from the site or on the support telephone number below.

|

| | | Contact us websupport@staalx.com or +1 (708) 697-3227

Follow StaalX on

|

| |

|

|

| |

.jpeg)