| | | |

Spot Prices Rise, Lead Times Extend

|

|

The domestic rebar market maintains a consistent theme of tight supply and sustained upward price pressure.

Mills continue to operate at capacity but are struggling to meet committed delivery schedules, pushing out lead times. While the domestic mills made no price increase announcements, import spot prices in Houston and the East Coast have recently moved up to align with current futures offers from importers. This supply constraint is expected to worsen before any major relief arrives, as the output from two anticipated new domestic mills is still some time away. Producers currently hold no floor stock, with the earliest available rolling schedules extending deep into December.

Wire Rod: Stable but Cautious

In contrast to rebar, the wire rod market appears more balanced, with current supply and demand levels matching. Domestic production has stabilized, notably with Liberty Steel’s Illinois mill returning to near-normal volumes.

Meanwhile, new import offers have slowed significantly. Importers face substantial regulatory challenges, ranging from high tariffs and potential new port charges (particularly for Chinese-flagged vessels) to volume disruption caused by the rebar anti-dumping cases (against Egypt, Algeria, and Vietnam). Despite the current stability, customer interest in Q1 shipments remains decent, reflecting caution that any domestic production disruption could quickly trigger another shortage situation.

Macroeconomic Headwinds: The Data Center Divide

The broader construction outlook for 2026 is trending pessimistically, according to the latest construction data.

The Associated Builders and Contractors (ABC) reports that backlogs for general contractors—specifically those operating outside the booming data center sector—have fallen by one-third. The data center construction segment is currently driving the majority of private non-residential activity and is essentially sustaining long-product demand.

However, this reliance is too close for comfort. Concerns are mounting that the capital pouring into AI infrastructure may represent a speculative bubble, and if the promised returns on these massive investments fail to materialize, those projects could cool off just as rapidly. The macro demand generated by AI technologies is keeping steel consumption afloat for now, but relying on a single vertical for long-term steel stability is a position of high vulnerability.

|

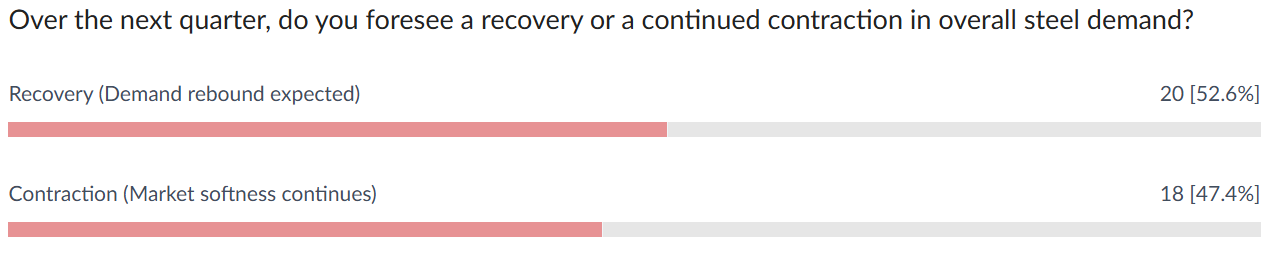

| | | Do you think the surge in data center construction will keep steel demand strong through 2026? |

| | | | | |

🎧 Missed Episode 4? Don’t fall behind — hear how government shutdown risks and the data center boom are reshaping the U.S. construction and steel markets. From project delays to material allocation shifts, Episode 4 dives into how these two powerful forces are pulling the industry in opposite directions.

|

| | | | |

⚙️ Steel Supply Is Tight — But Your Options Don’t Have to Be |

|

When imports slow and mills stay cautious, every quote counts. That’s where StaalX changes the game.

🔹 Real-time availability — Instantly check what’s in stock across domestic and import sources.

🚚 Instant freight quotes — Know your total landed cost before you buy.

💳 Flexible payment options — Keep your projects moving while protecting your cash flow.

From rebar to wire rod, mesh to merchant bars — StaalX makes sourcing faster, smarter, and simpler.

🎥 How to Use StaalX

Watch our quick walkthrough to see how easy it is to get quotes, make offers, and purchase steel directly online.

|

| | | | | From our content partner, SteelOrbis |

| | US import rebar and wire rod prices mostly steady on sluggish domestic demand, low imports continue

Thursday, 09 October 2025 19:44:23 (GMT+3) San Diego |

|

US import rebar and wire rod prices were mostly steady this week on a continuation of low domestic rebar and wire rod demand, even as imports remain reduced as a result of ongoing Section 232 steel tariffs, market insiders told SteelOrbis.

Long steel import insiders told SteelOrbis this week that suppliers in Malaysia and Vietnam are now offering “more competitive pricing” to compete with continued flat domestic supply, though most insiders expect domestic long steel pricing could remain mostly near current levels through the remainder of 2025.

“US mills are busy but not super busy,” remarked one US Gulf Coast long steel import insider, commenting on reports of continued tight supply, the result of ongoing 50 percent steel tariffs. “Most of the demand (for long steel) is being met by domestic mills, however, once lower October scrap numbers come out, we could see a slight reduction for domestic pricing.”

Insiders report limited import wire rod mesh supplies from Vietnam and Malaysia quoted on a DDP loaded truck basis on the US Gulf Coast at $42.00-43/cwt., ($840-860/nt or $926-975/mt), off from $42.50-43.50/cwt., one week earlier.

“Traders report no major import cargoes are set to arrive (in the US) until early 2026,” reported another US Gulf Coast insider. “This situation should result in more supply tightening, which could enhance resale margins for US distributors.”

Insiders told SteelOrbis domestic mills are offering lower pricing for October scrap as a way to preserve existing margins, even as domestic finished steel prices remain mostly flat.

“Domestic scrap prices are expected to decline $10-20/gt for October,” remarked another US Gulf Coast long steel insider. “This will offer cost relief to US mills and improve production margins without causing significant downward pressure on rebar.”

On the US Gulf Coast, import rebar as well as imported wire rod mesh on a CFR FO US Gulf basis is reported $20/ton lower at $590-600/mt, versus earlier reports at $610-620/mt. “Import offers from Vietnam and Malaysia are becoming more competitive,” the US import insider said. CFR pricing does not include Section 232 tariffs.

On the US East Coast, import rebar on a loaded truck basis is discussed at $45.00-46.50/cwt., ($900-930/nt or $992-1,025/mt), slightly higher on the low-side of the range versus the prior week’s $44.50-46.50/cwt., offers. Gulf Coast supply on a loaded truck basis was heard at $43.50-45.50/cwt., ($870-910/nt or $959-1,003/mt), depending on the size of the customer. “Import deliveries are a lot more tight on the US East Coast said one rebar insider. “As a result, people are expecting to pay higher prices because supply is more limited.”

Import insiders remain hopeful that this week’s meeting between US President Trump and Canadian Prime Minister Carney could represent a breakthrough for continuing Section 232 tariffs that have slashed US import activity.

“Carney was at the White House talking about a deal on metals with the US that could happen as quickly as possible,” an insider told SteelOrbis. “If there is a new tariff deal with Canada, it could change the import situation quite a bit. Canadian mills are really suffering,” he added. “If Canada gets back into the supply situation, maybe domestic pricing will soften.”

|

| US domestic rebar and wire rod flat for tenth straight week amid low demand, reduced October scrap

Friday, 10 October 2025 17:53:06 (GMT+3) San Diego |

| US domestic rebar and wire rod spot prices were flat for a tenth straight week as the market remains quiet amid continued low demand, and as scrap prices moved lower across all scrap grades, market insiders told SteelOrbis this week.

Continued maintenance operations at US mills are reducing the need for scrap, insiders said, causing settled prices to decline $10-20/gt across all grades from September levels.

Market respondents added that markets remained weak because the continued US government shutdown and its effects on construction project funding could cause rebar and wire rod demand to suffer. “Overall, we are going into a very significant slowdown,” a SteelOrbis import insider said. “The steel market is hopeful for next year, but I am still feeling pessimistic.”

In the weekly rebar spot markets, domestic supply on an FOB mill basis was assessed with most transactions noted at $44.50-45.50/cwt, ($890-910/nt or $981-1,003/mt), on average $45.00/cwt, ($900/nt or $992/mt), unchanged from seven days ago.

In the domestic wire rod market, domestic supply on an FOB mill basis was assessed with most transactions reported this week at $46.50-47.50/cwt ($930-950/nt or $1,025-1,047/mt), or an average of $47.00/cwt ($940/nt or $1,036/mt), unchanged from seven days ago.

Recent reports from wire rod insiders indicate Peoria, Illinois-based Liberty Steel's 700,000 ton Liberty Steel wire and rod plant is operating at or near capacity, reducing the likelihood of local near term price increases. “Liberty Steel has remained active this week,” the long steel insider said.

|

| US October scrap down $10-20/gt across all grades as maintenance culls demand

Thursday, 09 October 2025 20:49:52 (GMT+3) San Diego |

| US domestic scrap prices for the month of October are now seen settling lower across all scrap grades as a result of continued low demand from US domestic mills as units will likely remain shuttered for annual maintenance operations through November, scrap market insiders told SteelOrbis this week.

As October buy-cycle negotiations began in earnest this week, most survey respondents were certain that lower settled prices for prime and shredded scrap were likely as supplier inventories on the ground were reported adequate, and domestic mills appeared less apt to chase sideways pricing offers from suppliers as units remained shuttered for maintenance. At midweek, insiders reported to SteelOrbis that cut grades like P&S and HMS were also starting to trend at least $10-20/gt lower on a delivered basis.

“With the exception of Detroit, we would not be surprised to see the P&S (scrap) price drop by $20/gt,” remarked one Midwest scrap insider prior to settlement. “We expect HMS to settle $10 lower, shred to move down by $10/gt and primes to settle off by $20/gt as demand just isn’t there from the mills this month.”

Earlier this week, insider told SteelOrbis that prime scrap could settle $20-30/gt less, shreds $10-20/gt lower, while cuts were seen sideways to September settlements on a delivered to customer basis. Some insiders said that improved export demand for November scrap shipments this week overseas may have improved the October domestic scrap pricing outlook, limiting monthly declines and offering protection for US mills against lower production margins. Most obsolete grades were expected to settle $10-15/gt less at press time.

“Scrap export demand from Turkey, Egypt and Asia has strengthened, providing a global floor for US scrap,” remarked one US Gulf Coast long steel insider. “As a result, domestic scrap prices for October are expected to decline $10-20/gt, offering cost relief to US mills and improving production margins without downward pressure on rebar.”

“Pittsburgh is off $10/gt on shred and $20/gt on primes,” said one Gulf Coast scrap insider commenting on today’s (Oct. 9) settles.

Based on an average $20/gt decline expectation for delivered US Midwest prime busheling scrap in the US Ohio Valley, October busheling scrap is likely to settle at $395-420/gt, ($401-427/mt), while shredded scrap is seen settling near $365-370/gt ($371-376/mt). Ohio Valley P&S and HMS grades are last seen down $10-15/gt to September settles at $351-361/gt ($357-367/mt) and $315-335/gt ($320-340/mt), respectively, scrap insiders told SteelOrbis.

In the US Northeast, an overall lower October scrap settle could see prime busheling grade material traded on average $20/gt less on a delivered basis at $340-360/gt ($345-366/mt). Shredded grades are seen on average last $10/gt less at $315-325/gt ($320-330/mt), while obsolete grade HMS I/II is likely to settle $10/gt less than September at $295-310/gt ($300-315/mt), while P&S grade is seen $15/gt lower at $280-290/gt ($284-295/mt) delivered to mill, respectively, scrap insiders told SteelOrbis.

|

| |

Do you have any questions? Check out our FAQ! |

| Check out the most frequently asked questions about the service and products of StaalX. We are always here to chat with you in the chat boxes from the site or on the support telephone number below.

|

| | | Contact us websupport@staalx.com or +1 (708) 697-3227

Follow StaalX on

|

| |

|

|

| |

-article_image.jpg&w=1920&q=75)

.jpeg)