| | | | | |

Will 2026 Bring a Turnaround?

|

|

The U.S. steel market is flashing mixed signals, but a key metric—falling scrap prices—points toward a challenging environment for demand. The question on everyone’s mind is whether 2026 will bring the stability the industry desperately needs.

Import Tariffs Bite, But Domestic Struggle Continues

The recent doubling of steel tariffs to 50% has achieved its intended effect: U.S. steel imports saw a dramatic drop in September. Historically, the U.S. imports about 2 million metric tons of steel each month. According to the Steel Import Monitor, this quantity was nearly halved to about one million tons, effectively cutting the average volume by 50%.

Despite this massive reduction in foreign competition, many domestic producers are still struggling to fill their order books and raise prices.

For example, hot rolled flat rolled coils (HRC), a product that is typically more expensive than rebar or wire rod, is now being offered in the $40 cwt. range. This represents a $2 cwt. decrease since the tariffs were doubled. Our conversations with steel buyers over the last three months confirm a clear trend: most businesses are experiencing worsening sales conditions. With construction data and hiring also sagging, the industry may be heading in the wrong direction as the new year begins, a trend certainly not helped by continuing political adversity and trade uncertainty.

Rebar Bucks the Trend (For Now)

On a positive note, in the absence of foreign supply, rebar mills appear to be enjoying better-than-expected demand, no doubt fueled by the ongoing data center construction frenzy. Mills remain busy and are struggling to keep up with on-time deliveries for their orders.

However, an immediate price increase is unlikely. Scrap dealers are reporting a $10 - $20 per ton decrease for October. It would be a public relations nightmare for mills—already upsetting customers with delivery delays—to try and raise prices while their own costs are falling.

Given the scarcity of import sources right now, we may see an unusual, but not unprecedented, situation: import prices could surpass domestic prices late in the fourth quarter and early in the first quarter.

Wire Rods Await a Demand Rebound

For wire rods, domestic mills have found a nice pricing equilibrium, likely keeping their prices stable for the third consecutive month. While Asian mills are being more aggressive, the pricing difference isn't yet significant enough to cause an import surge. If domestic pricing remains stable, import volumes should remain a fraction of the average monthly volume from 2025.

The main question for the entire rod and wire market remains demand. Will it rebound in 2026?

It is increasingly looking like a challenging year for the wire industry unless the overall economy stabilizes, interest rates drop, and political and trade certainty returns.

|

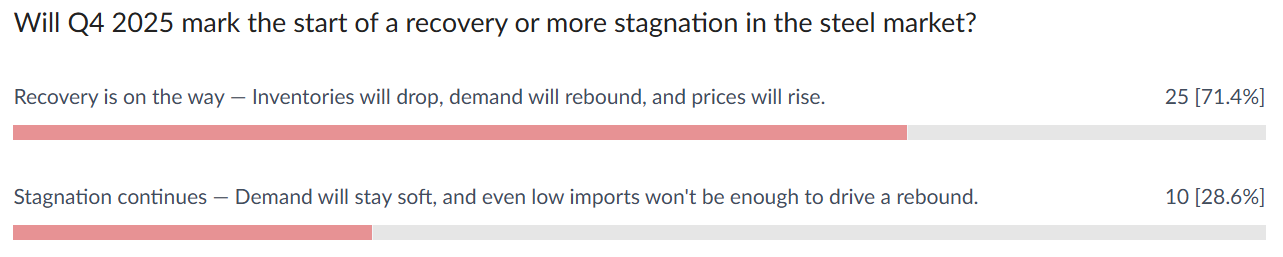

| | | Over the next quarter, do you foresee a recovery or a continued contraction in overall steel demand? |

| | | | | |

🎧 Missed Episode 3? Don’t fall behind — hear what’s driving the slowdown in construction and why steel imports are drying up.

|

| | | | |

Stop Leaving Money on the Table: The Smarter Way to Buy Steel is Here

In the world of construction, fabrication and manufacturing, profit margins are won and lost on material costs. For years, the process of procuring steel has been a complex dance of phone calls, opaque pricing, and a supply chain that adds costs at every step. Every dollar you overspend on rebar, wire mesh, or wire rod is a dollar taken directly from your bottom line. |

|

|

|

Business owners have a vested interest in buying better. But "better" doesn't just mean cheaper; it means smarter, faster, and more transparent. What if you could access top-tier pricing from master sellers without sacrificing service or quality?

That's why we built StaalX.

StaalX is a revolutionary online marketplace designed for one purpose: to make steel procurement more competitive. We connect you directly with the master sellers of rebar, wire mesh, and wire rod, cutting out the unnecessary layers of distribution that inflate your costs.

Our market analysis reveals a powerful truth: by leveraging the direct-from-source pricing on our platform, buyers can save an average of 8-15% on their steel purchases.

Consider the impact: On a $100,000 rebar order, that’s a direct saving of $8,000 to $15,000. On a $500,000 project, you could be adding up to $75,000 straight back into your business.

This isn't just a discount; it's a fundamental shift in how you acquire materials. It’s the difference between a good quarter and a great one.

While price competitiveness is our core advantage, StaalX provides a new venue for you to buy more efficiently without sacrificing service. Our platform offers: Unmatched Transparency: See prices from multiple vetted sellers in one place. Time Efficiency: Stop wasting hours on the phone chasing quotes. Find what you need, compare, and connect in minutes. Price Volatility Management: In a fluctuating market, knowledge is power. We invite you to check our platform, build a shopping cart with your typical order, and save it. You'll receive regular weekly pricing updates, allowing you to track the market and buy at the optimal time.

Don't let legacy purchasing habits erode your hard-earned profits. The opportunity to significantly enhance your profitability is here.

We invite you to visit StaalX today. Explore the listings for rebar, wire mesh, and wire rod. Save a cart to see firsthand how our weekly pricing updates can empower your purchasing strategy. Give StaalX a chance, and see how much you can save.

We look forward to seeing you soon! Murat Askin

|

| |

⚙️ Steel Supply Is Tight — But Your Options Don’t Have to Be |

|

When imports slow and mills stay cautious, every quote counts. That’s where StaalX changes the game.

🔹 Real-time availability — Instantly check what’s in stock across domestic and import sources.

🚚 Instant freight quotes — Know your total landed cost before you buy.

💳 Flexible payment options — Keep your projects moving while protecting your cash flow.

From rebar to wire rod, mesh to merchant bars — StaalX makes sourcing faster, smarter, and simpler. |

| | | | | From our content partner, SteelOrbis |

| | US import rebar and wire rod prices steady as domestic mills trim sales

Thursday, 02 October 2025 20:17:34 (GMT+3) San Diego |

|

US import rebar and wire rod prices remained steady this week, even as US mills -responding to reduced imports as a result of Section 232 steel tariffs- have begun reducing customer deliveries through allocations, market insiders told SteelOrbis.

On the US East Coast, import rebar pricing remained steady for yet another week, with local pricing maintaining its slight premium over the US Gulf Coast at $43-46.00/cwt., owing to reports of reduced August imports, insiders said. Importers say lower imports remain the primary reason for the East Coast price premium over the Gulf Coast.

Market insiders continue to report to SteelOrbis that reduced imports are tightening available supply, though mills have yet to raise prices for fear that increasing prices now could make imports a more attractive option versus domestic supply.

“The reports of tightness in the spot market are correct, and the mills are engaging in controlled order entry-allocation,” remarked one US East Coast rebar insider. The insider added that continued low finished steel demand from end-users could spur layoffs soon. “Fabricators and construction companies are looking at slower than normal activity with some talking about layoffs in the coming months if nothing changes.”

“Mills remain effectively sold out; prioritizing allocations,” remarked another US Gulf Coast insider. “Nucor, CMC, and Cascade are enforcing pricing discipline.”

As previously reported by SteelOrbis, preliminary import data from the Washington, D.C.-based International Trade Administration (ITA) suggests rebar and wire rod imports from abroad may have plunged sharply during the first half of September. And while final data will not be available from ITA until November, preliminary data shows September rebar imports plunged to a mere 8,967 mt, off from on average 60,000-70,000 tons per month, insiders said, while wire rod imports lagged at 21,936 mt, off from on average 80,000-90,000 tons per month. During August, 2025, preliminary ITA import data shows end-month rebar imports estimated at 57,812 mt, while wire rod imports were estimated at 91,331 mt. Final ITA August data is expected soon.

On the US Gulf Coast, import rebar is discussed unchanged at $43.00-45/cwt., ($860-900/nt or $948-992/mt), depending on the size of the customer, with most transactions averaging steady at $44.50/cwt. ($890/nt or $981/mt). While pricing remains stable, some insiders told SteelOrbis mills could announce another potential rebar price increase soon, especially if demand begins to rise.

Since steel import tariffs of 50 percent went into effect in June for the US’ primary suppliers Canada and Mexico, insiders tell SteelOrbis that domestic long steel supply, especially specific rebar sizes, has remained more limited. Wire rod supply has only recently been increasing as the 700,000 annual ton Peoria, Illinois-based Liberty Steel is reported at capacity.

“Liberty Steel is back at capacity,” said one Gulf Coast long steel insider. “The plant restart has covered earlier shortages, bringing balance, but also capping (price) upside.”

In the wire rod import segment, US Gulf Coast import supply on a DDP loaded truck basis is reported steady at $42.50-43.50/nt, ($850-870/nt or $937-959/mt). Domestic supply remained unchanged again at $46.50-47.50/nt ($930-950/nt or $1,025-1,047/mt). |

| US domestic long steel prices flat for ninth week as demand stumbles, scrap slips

Friday, 03 October 2025 19:38:39 (GMT+3) San Diego |

| US domestic rebar and wire rod prices were flat for a ninth straight week as spot market demand remains limited and as more scrap survey respondents told SteelOrbis this week that October scrap markets could continue to move lower.

Domestic rebar insiders said low spot demand and a lower scrap outlook is being balanced by continuing reports of reduced local supply as a result of ongoing 50 percent steel tariffs. Market respondents said September long steel imports “came down hard last month,” causing more uncertainty and a supply gap to develop in the steel market that continues to persist.

“September (preliminary) imports were closer to 10,000 mt when they are typically 80,000 mt which is causing a hole in the market,” a market insider explained.

In the weekly rebar spot markets, domestic supply on an FOB mill basis was assessed with most transactions noted at $44.50-45.50/cwt, ($890-910/nt or $981-1,003/mt), on average $45.00/cwt, ($900/nt or $992/mt), unchanged from seven days ago.

On the raw materials side, October scrap pricing across prime and now shredded US Midwest grades is now seen $10-30/gt lower. Insiders said obsolete grades may follow, though recent overseas scrap trades for November delivery indicate October domestic declines for HMS and P&S grades might be more limited.

One SteelOrbis long steel insider offered his take on the current long steel market situation. “After the additional 25 percent tariffs went into effect, domestic rebar mills basically went up 35 percent,” he said. “Steel fabricators got “squeezed hard by the short-term price increase,” he explained, causing an unanticipated delay in many pre-sold construction jobs. When many of those jobs came to a halt as a result of untenable material price increases, the current flat pricing situation was the result.

In the domestic wire rod market, domestic supply on an FOB mill basis was assessed with most transactions reported this week at $46.50-47.50/cwt ($930-950/nt or $1,025-1,047/mt), or an average of $47.00/cwt ($940/nt or $1,036/mt), unchanged from seven days ago. Little price movement in wire rod markets is likely near term as output from the key Liberty Steel wire and rod plant is reported to be at or near capacity.

“The Peoria (Illinois) plant’s 700,000 ton per year restart has covered earlier shortages, bringing balance but also capping upside (price movement),” another market insider reported to SteelOrbis. “Wire rod offers predictable pricing and secure supply,’ he said, “a safe planning base for distributors and fabricators heading into Q4.” |

| October US scrap now seen mostly down on reduced domestic mill demand, lower exports

Thursday, 02 October 2025 23:17:30 (GMT+3) San Diego |

| US scrap pricing forecasts for October moved lower this week on a combination of expectations for lower outage-related scrap purchases by domestic mills during October as plant maintenance continues, and because scrap export data from SteelOrbis reveals Turkish and other scrap buyers have reduced their appetite for US scrap as global steel demand wanes and countries enact more protectionist trade policies.

For the first week in the last four weeks surveyed, the expectation for reduced October scrap prices now includes Midwest shredded scrap grades, with a hint of lower pricing possible for obsolete scrap grades like HMS and P&S scrap. Scrap insiders also said early this week that domestic mills had begun canceling remaining September deliveries, a sure sign that mills expect lower prices could be forthcoming.

“It sounds like the scrap market is going to be down for October,” remarked one Midwest scrap insider. “Mills have started to cancel their September orders.”

“This week, primes are down $20-30/gt, while shred pricing is now also seen $10-20/gt lower,” another mill-based scrap buyer said. “There is very ample inventory, and reduced demand at mills in outage will drive prices down. Also, for the first time, we’ve also seen lots of shred offers in the Midwest this week.”

And, while obsolete scrap grades might be steady to down, insiders hinted a solid market expectation remains elusive until October buy-cycle negotiations begin in earnest next week.

As was previously reported by SteelOrbis, monthly customs data from the Washington, DC-based International Trade Administration (ITA) shows for the first seven months of 2025, exports of ferrous scrap to Turkey alone fell by nearly 19 percent from the equivalent period in 2024. And while there are currently no US tariffs on US steel scrap exports to Mexico and Canada -the US’ two primary trading partners- a 50 percent increase in import tariffs that began in June could indirectly impact exports of steel scrap, especially to Mexico, insiders say.

Near term, insiders predict domestic steel demand could continue to wane into the 4th quarter because historically, during the period from September through November, US mills perform annual maintenance operations, reducing theirs crap requirements as plants remain shuttered. One US contact told SteelOrbis late this week scrap pricing might rise late in the 4th quarter after planned maintenance ends and demand for scrap at mills improves.

SteelOrbis' sources overseas report that Turkish mills have begun seeking scrap cargoes for November shipments. Insiders say Turkey has a long way go before completing its purchases for this period. Scrap suppliers in both side of the Adriatic are offering higher prices to Turkish mills and managed to catch a slight increase during most recent bookings from the US and Baltic regions.

Based on this week’s updated October outlook, an average $25/gt decline expected for prime scrap grades could net a delivered US Midwest prime busheling scrap price in the US Ohio Valley at $390-415/gt ($396-422/mt), while shredded scrap at an average $15/gt decline, could settle near $360-365/gt ($366-371/mt) on a delivered basis. Ohio Valley P&S and HMS grades at current flat levels might trade for a fifth month at $361-371/gt ($367-377/mt) and $325-345/gt ($330-351/mt), respectively, SteelOrbis monthly scrap data shows.

In the US Northeast, prime busheling grade material could dip on average $25/gt to $335-355/gt ($341-361/mt), while shredded grades could tip $15/gt less at $310-320/gt ($315-325/mt). P&S and HMS grades could likely finish flat to potentially less at $295-305/gt ($300-310/mt) and 305-320/gt ($310-325/mt), respectively, to September settles, scrap insiders told SteelOrbis.

|

| |

Do you have any questions? Check out our FAQ! |

| Check out the most frequently asked questions about the service and products of StaalX. We are always here to chat with you in the chat boxes from the site or on the support telephone number below.

|

| | | Contact us websupport@staalx.com or +1 (708) 697-3227

Follow StaalX on

|

| |

|

| |

-article_image.jpg&w=1920&q=75)

.jpeg)