Nucor recently announced a $35 per short ton price increase for its beam and piling products. This move signals strength in the structural steel market. The increase comes even as scrap prices, a key cost driver for steel mills, have remained stable. The closely watched Chicago Shredded Index showed no change in September for the fifth consecutive month. This stability in raw material costs allows mills to increase prices based on demand and market positioning rather than being pressured by rising input costs.

Rebar and Wire Rod: The tug-of-war between supply and demand.

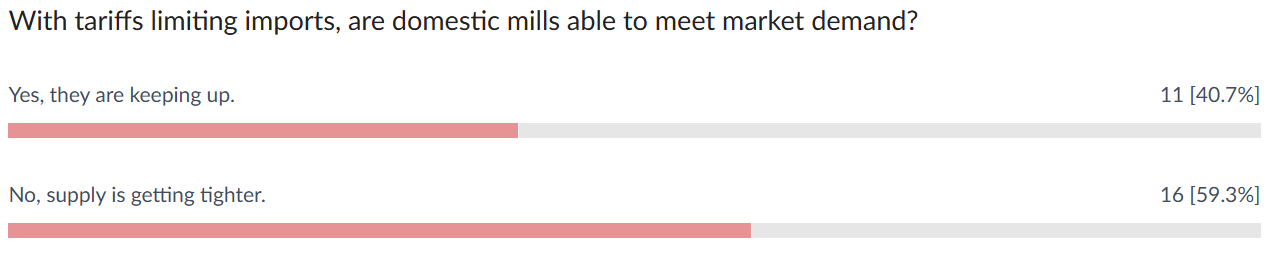

While the beam market is seeing an uptick, the outlook for other long products is more varied. Rebar: Despite no announcements yet from the rebar producers, rebar prices may still see an increase in September. This is primarily due to a tightening supply, a result of a sharp decline in imports. The imposition of doubled steel tariffs, combined with a new antidumping filing in June, has created significant trade obstacles. Only a few foreign mills that can produce steel to the required ASTM sizes and standards are free from these new cases, but they have not historically been regular exporters to the U.S. market. With the 50% tariff, foreign mills would need to offer substantial discounts to compete with domestic prices. While construction demand for rebar is not booming, it is solid enough to keep domestic mills operating at a healthy capacity.

Wire Rod: The wire rod market has also been impacted by supply changes. The Liberty Steel plant in Illinois has resumed production and is fulfilling orders, despite facing significant financial challenges. This re-entry to the market is helping to fill the void left by a slowdown in imports. Canadian imports, for example, have dropped from monthly levels of 40,000 metric tons to below 15,000 metric tons in August. It is believed that most of the remaining imports are higher-grade products like cold heading and electrode qualities.

The Economic Backdrop: Interest Rates and Construction Outlook

The broader economic environment is also playing a role. The Federal Reserve is widely expected to lower interest rates by 25 basis points this week. While a modest adjustment, this could be the first of several rate cuts by the end of the year, potentially stimulating economic activity.

Supporting a positive long-term outlook for the construction sector is the Dodge Momentum Index, which registered its third consecutive month of expansion. This suggests a significant pipeline of projects for the latter half of 2026 and beyond. A robust construction market could strain the capacity of domestic steel producers if demand truly rebounds. However, the potential for policy-related headwinds, such as ongoing trade and immigration issues, could still dampen market growth. Importers, for their part, are likely in a holding pattern, waiting to see if domestic price increases create an opening for them to re-enter the market.

|

-article_image.jpg&w=1920&q=75)