| | | |

The Last of Major Import Volumes?

|

|

The U.S. rebar and wire rod market is witnessing a significant shift as the final major import volumes, primarily from Vietnam, are observed. Import statistics for August show a notable drop in overall wire rod and rebar imports. A substantial portion of August's entries, including 25,000 metric tons of wire rod and 30,000 metric tons of rebar, originated from Vietnam. These shipments are likely the last to arrive, having been booked before the June 4th doubling of tariffs to 50%. Given the two-month sailing time and potential port delays, a significant decline in Vietnamese and other steel imports is expected going forward.

The higher, unexpected tariffs on these incoming shipments have created challenges for traders. However, a recent rise in spot prices since June —from $37-$38 per cwt to $42-$43 per cwt for rebar in Texas—has helped importers stay afloat.

Domestic Market: Strain and Uncertainty

As imports become more challenging, the domestic market is showing signs of strain. Domestic rebar availability is limited, and fabricators are growing nervous about heading into the fourth quarter with insufficient inventory. Meanwhile, mills are reportedly struggling to meet delivery commitments and are operating on extended rolling schedules.

The wire rod market, however, presents a different scenario. There is no urgency to fill inventory gaps; in fact, some wire drawers have accumulated excess stock due to softening sales. Liberty Steel and Wire in Peoria, IL, is back in production and fulfilling orders without major setbacks. Yet, despite this domestic supply, there's a collective uncertainty among wire drawers about whether demand will pick up for the 2026 spring season. If it does, they recognize that domestic production may not be enough to satisfy the need for restocking.

Economic Headwinds and Future Outlook

The broader economic environment continues to be a concern. Manufacturing, despite political promises, has not seen a surge in activity and has actually been losing jobs. Recent reports indicate that the U.S. economy added far fewer jobs than expected in August, with manufacturing and construction being among the sectors with job losses. This overall economic slowdown has sparked speculation that the Federal Reserve may begin reducing interest rates, but many in the industry fear it may be "too little, too late" to provide meaningful help.

Seismic shifts are needed in the supply chain, but uncertainty persists. While the focus on domestic manufacturing and "onshoring" is a key policy, significant investments in the downstream steel-consuming sector have yet to materialize.

|

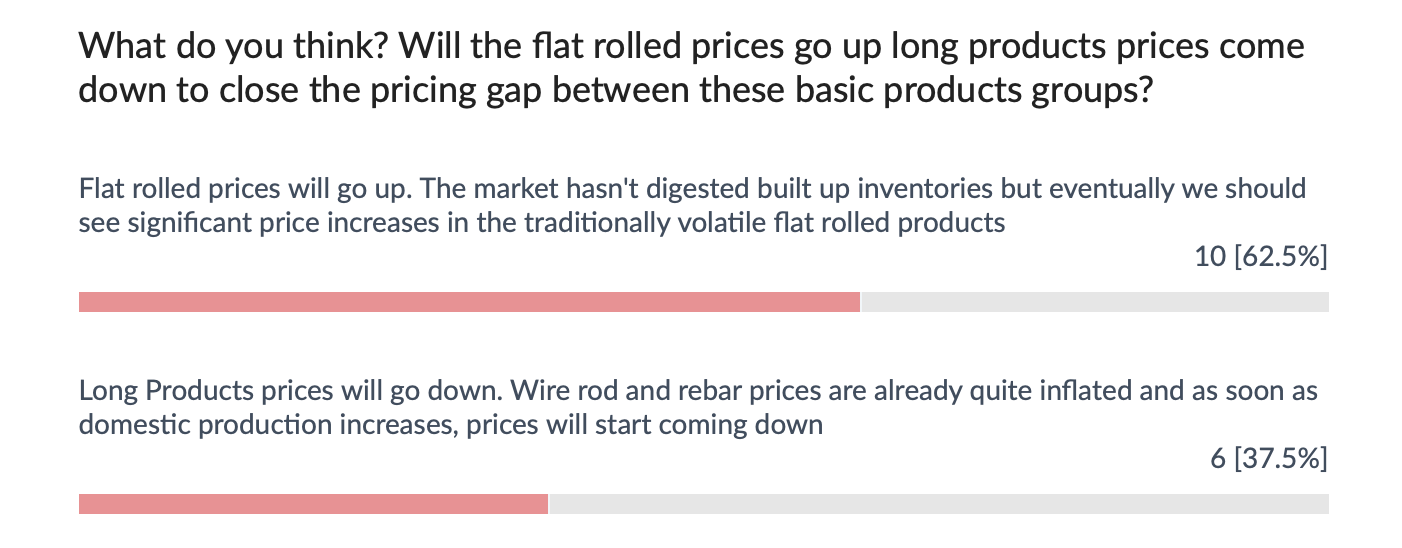

| | | With tariffs limiting imports, are domestic mills able to meet market demand? |

| | | | |

StaalX' Marketplace Model

There are quite a few e-commerce models and a lot of people asked me about the StaalX model. Unlike a traditional agent or a pure marketplace, StaalX buys from a seller and sells to a buyer directly, assuming the role of a principal. This approach fundamentally addresses the core B2B challenges of trust and credit risk. |

|

|

|

By taking on the financial and logistical burden, StaalX provides a level of security and simplicity that is otherwise difficult to achieve when trading with new, unknown partners. It eliminates the need for buyers and sellers to conduct extensive onboarding or credit checks on each other.

A pure, hands-off marketplace model, a staple of consumer e-commerce, is incompatible with the complexities of the steel industry. Trust is the single most critical currency in the B2B steel industry, where a single transaction can be worth hundreds of thousands or even millions of dollars. Simply deep trust is required for high-value transactions and the buyers will need to know that their orders will be fulfilled without worrying about the seller's performance. StaalX guarantees the success of the transaction.

Of course, there are other benefits of this model as not all sellers in the steel market want to be on an open platform, listing and offering products that may not be welcomed by their traditional customers. With our model, sellers enjoy anonymity and freely discount when they need to move their obsolete inventory. Buyers reap the benefits.

This is our current marketplace model for the material on the ground and ready for immediate shipment. StaalX is also working on another model, codenamed StaalX NeXt for future bookings of orders, including domestic and import future rollings and shipments, one, two or more months down the line deliveries. The model will likely adopt a transparent relationship between buyers and sellers and StaalX will fulfill the role of logistics, customs clearance and finance as a service, and making transactions easier, as our corporate mission dictates.

Stay tuned for that and check out our current offers at StaalX.com.

|

| |

🚛 StaalX puts control in your hands |

| Steel sourcing made simple.

✅ Live inventory & pricing — always up-to-date

✅ Instant delivery windows & freight quotes

✅ Easy, Amazon-style checkout

✅ Tools that simplify your workflow

🔗 Ready to experience it? Visit www.staalx.com

📦 Rebar. Wire rod. Mesh. It’s all a click away.

|

| | | | | From our content partner, SteelOrbis

|

| |

US domestic rebar and wire rod both flat this week Thursday, 11 September 2025 17:50:44 (GMT+3) San Diego

US domestic rebar and wire rod are both flat this week as scrap stays sideways in September. US imports are low and the current demand is not competitive along with slower construction and economy.

In the weekly rebar spot markets, domestic supply on an FOB mill basis was assessed with most transactions noted at $44.50- 45.50/cwt, ($890-910/nt or $981-1,003/mt), on average $45.00/cwt, ($900/nt or $992/mt), unchanged from seven days ago.

In the domestic wire rod market, domestic supply on an FOB mill basis was assessed with most transactions reported this week at $46.50-47.50/cwt ($930-950/nt or $1,025-1,047/mt), or an average of $47.00/cwt ($940/nt or $1,036/mt), unchanged from seven days ago. “Liberty Steel has been tipping up their delivery prices which is keeping the wire rod prices stable,” said a SteelOrbis insider.

October US scrap outlook seen mixed in early call following steady to lower September settles

Thursday, 11 September 2025 20:08:06 (GMT+3) San Diego October US scrap pricing is seen mixed this week following the recent steady to lower settles posted in the September scrap market, insiders told SteelOrbis this week. While one group of respondents to a SteelOrbis survey sees October scrap potentially higher as a result of increased long steel production in the late-3rd and 4th quarters -which could require more scrap- the other camp points to continued low US scrap demand, plentiful mill inventories (especially busheling) and an expectation for low US East Coast export requirements next month as a key reason for a lower October scrap pricing expectation.

During the recent September monthly buy-cycle negotiations, US scrap grades -with the exception of prime scrap grades- settled sideways for a fourth month. Prime grades only, settled $20/gt lower as a result of reports of plentiful busheling inventories at mills and continued low demand expectations, market insiders told SteelOrbis.

“US Midwest shredded scrap, which is most important for rebar production, closed the month sideways again for a fourth month,” said one US Midwest long steel importer that follows US scrap pricing following the September settlement. “There’s just not much moving on scrap,” he said. “Markets should pick up soon as more people return from vacations, however, the US economy continues to show signs of slowing down as more deportations happen and lower job numbers reflect a further slow down in construction activity.”

Last week, insiders told SteelOrbis that yearly mill maintenance programs that begin in September and typically end in November would limit local mill scrap buys during the September scrap negotiations. They added that prime supply remains abundant since mills were expected to buy more prime scrap during August supply negotiations because many mill buyers expected US President Trump to follow though on threats to implement 50 percent tariffs on Brazilian pig iron, a key component of US steel production. Once Trump later recanted on the threats -and mills failed to buy- suppliers found they had too much prime supply on hand. Insiders also added that continued declines in US flat steel pricing also were not supportive of domestic scrap.

“Our longer-term indicators are turning bullish,” said one US Gulf Coast- based long steel insider. “Scrap is stable short-term, but it is expected to strengthen into late-Q4-Q1 2026, as (long steel) mills ramp up production and inventories thin.”

“We’re hearing strong sideways for October,” said another US East Coast scrap supplier, who was unwilling to supply a reason for the increased price expectation.

“Sideways to down is looking more realistic to me,” lamented another US Gulf Coast market insider, reflecting on reports of a potential recovery in scrap pricing for October. “The Turks are not buying much scrap due to continued weak demand.”

Today, export market insiders told SteelOrbis the Turkish market was surprised when an Izmir-based mill bought and ex-Netherlands cargo for October shipment of HMS I/II 80:20 scrap at $337 CFR TR, sharply below earlier reported trades.

“This means ex-US pricing could drop to $335/mt CFR, TR, which is $7/mt lower than the most recent ex-US deals done in Turkey, so negative sentiment persists,” the insider said.

During September scrap buy-cycle negotiations, following three months of steady pricing, US Midwest prime busheling scrap in the Ohio Valley, settled $20/gt lower at $415-440/gt ($423-448/mt), while shredded scrap settled flat to August at $375-380/gt ($381-387/mt). Ohio Valley P&S and HMS grades traded flat for a fourth month at $361-371/gt ($367-377/mt) and $325-345/gt ($330-387/mt), respectively, SteelOrbis monthly scrap data shows.

In the US Northeast, prime busheling grade material settled $20/gt less at $360-380/gt ($367-387/mt), while shredded grades settled flat to August at $325-335/gt ($330-342/mt). P&S and HMS grades finished sideways to the $295-305/gt ($300-310/mt) and 305-320/gt ($310-325/mt), respective August settles, scrap insiders told SteelOrbis this week. |

| |

Do you have any questions? Check out our FAQ! |

| Check out the most frequently asked questions about the service and products of StaalX. We are always here to chat with you in the chat boxes from the site or on the support telephone number below.

|

| | | Contact us websupport@staalx.com or +1 (708) 697-3227

Follow StaalX on

|

| |

|

|

| |