|

StaalX' Marketplace Model

There are quite a few e-commerce models and a lot of people asked me about the StaalX model. Unlike a traditional agent or a pure marketplace, StaalX buys from a seller and sells to a buyer directly, assuming the role of a principal. This approach fundamentally addresses the core B2B challenges of trust and credit risk. |

|

|

|

By taking on the financial and logistical burden, StaalX provides a level of security and simplicity that is otherwise difficult to achieve when trading with new, unknown partners. It eliminates the need for buyers and sellers to conduct extensive onboarding or credit checks on each other.

A pure, hands-off marketplace model, a staple of consumer e-commerce, is incompatible with the complexities of the steel industry. Trust is the single most critical currency in the B2B steel industry, where a single transaction can be worth hundreds of thousands or even millions of dollars. Simply deep trust is required for high-value transactions and the buyers will need to know that their orders will be fulfilled without worrying about the seller's performance. StaalX guarantees the success of the transaction.

Of course, there are other benefits of this model as not all sellers in the steel market want to be on an open platform, listing and offering products that may not be welcomed by their traditional customers. With our model, sellers enjoy anonymity and freely discount when they need to move their obsolete inventory. Buyers reap the benefits.

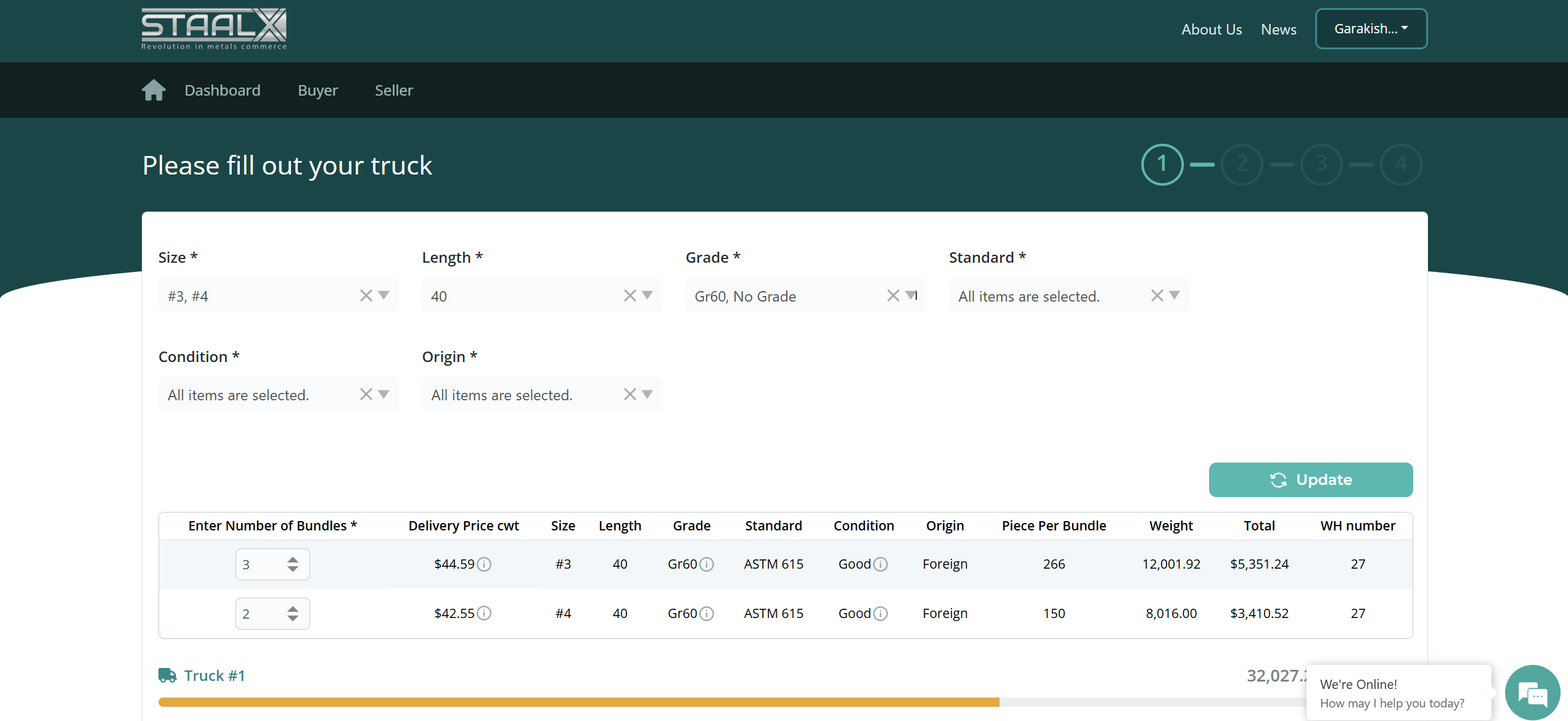

This is our current marketplace model for the material on the ground and ready for immediate shipment. StaalX is also working on another model, codenamed StaalX NeXt for future bookings of orders, including domestic and import future rollings and shipments, one, two or more months down the line deliveries. The model will likely adopt a transparent relationship between buyers and sellers and StaalX will fulfill the role of logistics, customs clearance and finance as a service, and making transactions easier, as our corporate mission dictates.

Stay tuned for that and check out our current offers at StaalX.com.

|

| | | | |

The U.S. rebar market is currently in a puzzling state. Despite a seemingly troublesome outlook for the broader construction sector, the rebar market is experiencing a tight supply situation, with most domestic mills reporting near-zero floor stock. How did we arrive at this point?

The challenges in construction are undeniable. A crackdown on immigration has led to a significant labor crunch, with nearly 45% of contractors citing workforce issues as a cause of project delays. Additionally, 16% of contractors are reporting project impacts related to tariffs. Rebar fabricators confirm this trend, noting that while they are estimating a high volume of projects, fewer are actually moving forward. High interest rates are also a major headwind, and it is unlikely they will drop fast enough this year to have a material impact on project costs. While the overall construction activity is seeing some contraction, it remains at a decent level, effectively absorbing available supply despite these self-imposed obstacles.

On the import front, rebar offers are scarce. Ongoing antidumping duties have severely limited options, and the few offers that exist are priced very close to what large domestic buyers—fabricators and master distributors—are paying. This lack of a significant price advantage means that imported rebar is not gaining much traction. This has also widened the gap in buying prices between small and large domestic purchasers, with preferential pricing becoming more common.

Long Products Market Dynamics

The wire rod market is notably calmer. Following Nucor's decision to hold prices steady and a stable scrap market, major price shifts are not anticipated in the near term.

However, the import environment for wire rod is becoming increasingly challenging. While there is interest in Q1 2026 arrivals, it is getting harder to put together shipments and volume. Some major wire rod exporters to the U.S. have been hit by rebar antidumping cases, and this has complicated their ability to make combined shipments, making the import landscape for rods significantly more difficult.

Looking Ahead

The divergence in pricing between long products and flat-rolled products has been a notable market quirk this year. Since the doubling of Section 232 tariffs in June, long product prices have been on the rise while flat-rolled prices have moved in the opposite direction. This can be attributed to increased domestic flat-rolled production, which has intensified competition among U.S. mills rather than with imports.

This dynamic may be short-lived for rebar. New domestic production capacity from Hybar, CMC and Nucor is scheduled to come online in Q4 2025 and Q1 2026. This influx of supply is expected to ease the current shortage and could potentially lead to a price correction in the near future.

|

| | | What do you think? Will the flat rolled prices go up long products prices come down to close the pricing gap between these basic products groups? |

| |

🚛 Steel Buying, Reimagined. |

| Sick of the back-and-forth?

The future of steel sourcing is already here — and it’s faster and built for you.

Why buyers are switching to StaalX: ✅ Live pricing — no more quote requests

✅ Instant freight costs & delivery windows

✅ Amazon-style checkout — for rebar, mesh & wire rod

✅ Built-in tools that make fabricators' lives easier

🔗 Ready to experience it? Visit www.staalx.com

📦 Rebar. Wire rod. Mesh. It’s all a click away.

|

| | | | | From our content partner, SteelOrbis

|

| | US import rebar and wire rod prices still strong amid trimmed supply, local shortages Friday, 29 August 2025 14:23:59 (GMT+3) San Diego US import rebar and wire rod pricing has continued steady to higher amid continued low imports and as reports of local supply shortages persist, market insiders told SteelOrbis this week.

Insiders continue to lament that the combination of ongoing 50 percent steel import tariffs and the enhanced importer risk associated with ongoing antidumping cases currently under review by the US Department of Commerce (DOC) continues to limit the amount of import material being made available as an alternative to domestic supply. As domestic prices continue to rise, however, imports may be beginning to look more favorable.

“Supply availability is getting tighter and US mills are getting busier, so some limited imports may begin to be possible,” remarked one US Gulf Coast long steel insider to SteelOrbis. “Availability could be a developing issue in certain parts of the country where import product was predominantly sold,” said another long steel insider. “The US West is a bit more competitive,” he added.

Another SteelOrbis long steel importer source commented that shortages of rebar continue to become more frequent in parts of south Texas, with talk of supply allocations on existing supply contracts from domestic mills in the US Southeast beginning to be heard. Meaningful rebar supply relief from the Osceola, Arkansas-based Hybar rebar mill is not expected to be seen in the market until the fourth quarter, he said.

The same source added, “We’re seeing rebar imports at record lows with July licenses reported at 34,051 metric tons, down 73 percent month on month, with August pacing at 44,510 metric tons as of August 18. Domestic mills are running at high capacity of around 800,000 tons per month, but they continue to restrict spot orders in order to protect spot pricing markets.”

This week, import rebar on a loaded truck basis on the US Gulf Coast is discussed at $40-45/cwt., ($800-900/nt or $882-992/mt), depending on the size of the customer, with most transactions averaging $1.00/cwt. higher at $44.50/cwt, up from $43-44/cwt. ($860-880/nt or $948-970/mt), or on average $43.50/cwt. one week prior. Insiders said shortages in south Texas have caused some local suppliers to raise price offers toward $46-47/cwt, though it remains unclear whether buyers are interested yet.

On the US East Coast, import rebar gained a bit less again this week versus the Gulf Coast, insiders said, with most transactions averaging at $42-46/cwt., depending on customer size, settling the week about $0.50/cwt. higher at on average $45.00/cwt. ($900/nt or $992/mt). Reports persist of shortages of some sizes of rebar product as imports wane and domestic mills struggle to fill a growing supply gap by boosting output.

In the import wire rod markets, import wire rod offers in the Port of Houston are heard at $44-49/cwt. ($880- 980/nt or $970-1,080/mt) inclusive of tariffs, though most are deemed non-viable compared with domestic mesh trades heard flat this week at $42.50-43.50/cwt. ($850-870/nt or $937-959/mt).

“Since Nucor attempted a $20/ton increase in wire rod pricing in July, traction in the market has remained limited,” one Mexican long steel insider told SteelOrbis. “We’re seeing lead times for domestic wire rod at five to six weeks with demand fairly steady but not strong as a result of tariffs,” he added. “Imports remain scarce keeping supply balanced despite sluggish consumption as buyers continue to wait for lower interest rates before stepping up their orders.”

Recent industry reports from this week’s SMU Steel Summit in Atlanta, Georgia, indicated there is currently an 80 percent certainty in financial market circles that the US Federal Reserve will lower the over-night bank lending rate by a one-quarter point at the next Fed Open Market Committee meeting on September 16-17. Rates have remained at 4.25-4.50 percent since December 2024 and have been blamed for a general lack of investment in US infrastructure projects.

In the Mexican long steel markets, while 50 percent tariffs remain in place, pre-tariff rebar available in the vicinity of Houston, Texas, on a loaded truck basis is little changed at $40-42/cwt. ($800-840/nt or $937/mt to $959/mt), compared with earlier weekly estimates at $40-43/cwt., insiders said. As Mexico continues to deal with high export tariffs to the US, one Mexican trader told SteelOrbis that their direct sales of long steel to Canada via ship and rail have increased fourfold, helping to support recent local Mexican price stability in the face of unremarkable demand.

Local US rebar and wire rod prices stable for fifth straight week Friday, 29 August 2025 17:09:36 (GMT+3) San Diego US domestic rebar and wire rod prices have remained unchanged this week as scrap stays sideways to lower. Domestic availability in the US is being discussed as an issue where import products are predominantly being sold. Transitioning to September, the steel market should start to move out of the “summer doldrums” reported last week.

In the weekly rebar spot markets, domestic supply on FOB mill basis was assessed with most transactions noted at $43.50-44.50/cwt ($870-890/nt or $959-981/mt), on average $44.00/cwt, ($880/nt or $970/mt), unchanged from seven days ago. “The domestic rebar is expected to move slightly higher next week,” according to a long steel contact.

In the domestic wire rod market, domestic supply on FOB mill basis was assessed with most transactions reported this week at $46.50-47.50/cwt ($930-950/nt or $1,025-1,047/mt), or an average of $47.00/cwt ($940/nt or $1,036/mt), unchanged from seven days ago.

September US scrap seen sideways to down for third week amid declining flat steel, start of maintenance season Thursday, 28 August 2025 23:36:01 (GMT+3) San Diego The outlook for September US scrap pricing next month remained unchanged for a third week at sideways to potentially lower this week as a result of continued reports of low flat steel pricing as well as new reports that September-November mill maintenance programs could further limit local mill scrap buys during the September buy-cycle negotiation period next month, market insiders told SteelOrbis. Reports of a continued prime scrap “overhang,” the result of reduced mill purchases of prime scrap during August supply negotiations continued, but to less an extent than were heard the week prior.

“We’re expecting to see scrap coming off a bit in September as supply is steady although demand is likely to fall as a result of the annual mill outage season,” remarked one US Midwest-based mill scrap buyer. “We’re not expecting anything dramatic, but, we could see prime scrap trade off between $10-20/ton.”

“There’s really not anything new out there on the consensus for September scrap” said another Gulf Coast scrap insider. “We’re seeing the status quo, as there appears to be some downside pressure on primes. We’ll see if that happens, but, all other grades are anticipated to trade sideways to August.”

One US East Coast scrap insider begged to differ on reports of a continued prime scrap supply overhang in his local scrap region.

“I would agree that September scrap could settle soft-sideways next month on low demand,” he said. “But, I personally haven’t seen a lot of supply overhang for busheling.”

Insiders told SteelOrbis in earlier reports that US mills didn’t buy the prime scrap that local scrap suppliers had expected them to purchase during the August buy-cycle because threatened 50 percent tariffs on Brazilian pig iron by US President Trump failed to occur. An insider remarked “I think mill closures across September, October and November will create significant downward pressure on pricing during the September and October buys,” he said last week. “Especially with the expectation of a continued bearish export market and the softness in hot-rolled coil pricing.”

This week, US Midwest flat steel pricing continued lower amid reports of trades done at $5/nt less on average $820/nt ($904/mt), or $41.00/cwt., off from an average $820-$830/nt ($904-915/mt), or on average $41.25/cwt., seven days earlier. Flat steel insiders said HRC pricing could be nearing a bottom at about $800/nt ($882/mt) or $40/cwt., as reports emerge of improved domestic demand seen by mills.

“We see positive things regarding demand,” said Nucor Corporation Executive Vice President of Sheet Products, Noah Hanners, at this week’s SMU Steel Summit conference in Atlanta, Georgia, when asked about this week’s Consumer Spot Price (CSP) increase for hot-rolled coils, the first reported by the key US mill in three weeks to $875/nt ($965/mt) or $43.75/cwt. “This week’s price increase has nothing to do with tariffs at all, but rather we see a developing backlog of orders coming from customers, which is supportive of demand.”

Another SteelOrbis flat steel contact remarked, “There is a mix of opinions in the marketplace right now, however, there is a general feeling that demand is going up in certain sectors as people return from vacations,” he said. “The mills definitely have felt an increase of volume on quotes, but companies are looking for lower prices and mills are not closing orders,” he added. “Scrap values are staying the same versus prices that are coming down, so that is reducing margins with the mills. To me it feels like HRC prices will not decline below $800/nt.”

Given this week’s continued declines in spot flat steel pricing, SteelOrbis historical data shows price levels have declined consistently since the end of June as scrap demand has remained unremarkable with sideways pricing reported for three straight months.

Based on a sideways to down from August, September settlement, US Midwest prime busheling scrap in the Ohio Valley could settle at or below $435-460/gt ($443-468/mt), while shredded scrap might settle at or below $375-380/gt ($381-387/mt). Ohio Valley P&S and HMS grades are seen at or below $361-371/gt ($367-377/mt) and $325-345/gt ($330-387/mt), respectively, scrap insiders told SteelOrbis.

In the US Northeast, a sideways to potentially lower September scrap settle would put prime busheling grade material at or below $380-400/gt ($387-407/mt), while shredded grades could settle at or below $325-335/gt ($330-342/mt). P&S and HMS grades might finish at or below $295-305/gt ($300-310/mt) and 305-320/gt ($310-325/mt), respectively, scrap insiders told SteelOrbis this week.

|

| |

Do you have any questions? Check out our FAQ! |

| Check out the most frequently asked questions about the service and products of StaalX. We are always here to chat with you in the chat boxes from the site or on the support telephone number below.

|

| | | Contact us websupport@staalx.com or +1 (708) 697-3227

Follow StaalX on

|

| |

|

|

| |

-article_image.jpg&w=1920&q=75)