US domestic rebar and wire rod pricing flat on week though prices could trend lower near term

Thursday, 24 April 2025 20:45:19 (GMT+3) San Diego

US domestic rebar and wire rod prices were flat this week, though pricing could trend down in the near term, as domestic demand remains weak and US scrap prices are seen lower for May, long steel market insiders told SteelOrbis.

Following lower April price settles, US Midwest May prime and shredded scrap prices are expected to settle between $10-30/gt ($10-30/mt) less during monthly supply negotiations, owing to continued reports of plentiful supply at local yards and reduced domestic and international demand for new scrap.

In the weekly rebar spot markets, domestic supply on an FOB mill basis is assessed with most transactions noted at $38.00-39.50/cwt. ($760-790/nt or $838-871/mt), on average $38.75/cwt. ($775/nt or $854/mt), unchanged from seven days ago.

"Buyers are taking a very conservative approach to buying steel at the moment," said one SteelOrbis long steel insider. "With recent decrease in purchases, domestic rebar and wire rod pricing has stayed very steady for several weeks now," he said.

In the domestic wire rod market, most transactions were reported this week at $45.50-46.50/cwt. ($910-930/nt or $1,003-1,025/mt), or an average of $46.00/cwt. ($920/nt or $1,014/mt), unchanged from seven days ago. Insiders report that the downed Liberty Steel wire and rod plant remains offline, so domestic supplies remain tight, even as wire rod demand struggles.

Insiders said that like the recent rally in flat steel pricing, long steel pricing increases appear to have moderated, partly the result of reduced prices seen for April and May scrap amid reduced mill demand for finished steel and partly the result of recent actions by the US Trump administration on implement 25 percent tariffs on imported steel and aluminum. Continued uncertainty over tariffs, the contacts say, is preventing longer-term investments in infrastructure projects that normally increase yearly demand for long steel products like rebar and wire rod.

"People seem to be also taking a more conservative approach to infrastructure project starts,” the insider added. "With the tariffs in place, US mills are likely to start lowering their prices to retain market share in the face of imports."

US import rebar and wire rod pricing flat to down with declining US May scrap, tariff and shipping concerns still an issue

Thursday, 24 April 2025 20:55:33 (GMT+3) San Diego

US Import rebar and wire rod pricing was steady to lower this week amid a growing market outlook for lower US scrap pricing for May, amid continued concerns over steel tariffs and issues with the movement of commodities on Chinese ships, market insiders told SteelOrbis.

Insiders said imports into the US are likely to remain minimal in the near term because many countries previously exempt from tariffs under the Biden administration are now subject to minimum 25 percent import tariffs on steel and aluminum.

"As US scrap prices decline for May, even as domestic supplies remain tight with the Liberty plant still offline, it is questionable whether these current prices are sustainable," said one long steel import insider. "Like what we saw in US flat steel pricing, I'm hearing long steel pricing remains fairly stable, but leaning lower," he said. "We may have peaked for now on long steel import pricing."

Imported rebar on a loaded truck basis at the US Gulf Coast and US East Coast remains flat amid limited US demand at $36.50-38.50 cwt. ($730-770/nt or $805-849/mt), or on average $37.50/cwt., versus $37.00-38.00/cwt. ($740-760/nt or $816-838/mt) three weeks earlier. May import shipments from Egypt, Algeria and Vietnam for June-July delivery into the US Gulf Coast are discussed flat yet again at $38.00-39.00/cwt. ($760-780/nt or $838-860/mt).

In the Mexican long steel export market, trading remains quiet and slow as 25 percent tariffs limit available trade opportunities. Import rebar on a loaded truck basis vicinity Houston, Texas, from available US stock is reported slightly lower at $36.75-38.75/cwt. ($735-775/nt or $810-854/mt), versus week-earlier trades at $37.00-39.00/cwt. ($740-780/nt or $816-860/mt), market insiders told SteelOrbis.

The import insider added that as Section 232 steel tariffs of 25 percent are now in effect, import shipments on rebar from North Africa, Malaysia, and Vietnam are likely to rise as buyers adjust their supply chains to make up the supply shortfall from previous lower-priced sales originating out of Bulgaria and the Ukraine. Those steel deliveries were previously exempt from import tariffs. "While some import buyers are not booking because of the tariffs, we're not yet seeing a shortage of sales out of Egypt," he said. "However, we are expecting to see a price correction later in April or May."

In other import rebar markets, pricing for import rebar on a CFR, free-out basis at the US Gulf Coast was discussed on average $5/mt ($5/nt) less at $615-635/mt, off from $620-640/mt one week earlier. Insiders said June scrap prices could be bolstered as increased purchases are made to cover the rebar production that is expected to commence at the new 600,000 ton per year Hybar rebar mill in Osceola, Arkansas.

The price of imported wire rod mesh on a DDP loaded truck basis remained flat this week as a result of solid domestic sales, even as the status of the downed Liberty Steel plant remains uncertain. Pricing is last assessed unchanged at $37.50-39.50/cwt. ($750-790/nt or $827-871/mt).

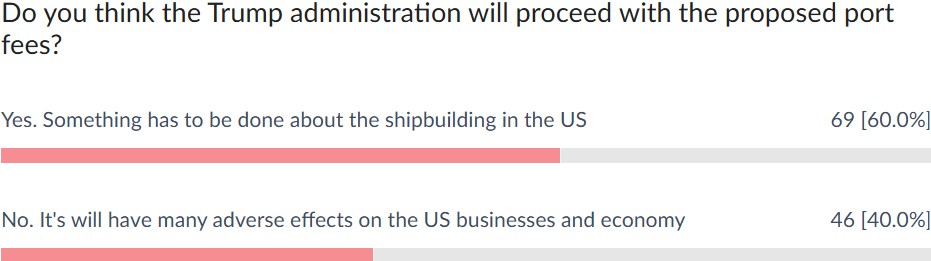

"The shipping markets are in a tense calm,” remarked another Gulf Coast long steel importer to SteelOrbis. Recently, US president Trump released a plan through the US Trade Representative to assess Chinese ships a $50/nt fee based on a ships gross weight. The fee, which may go into effect on October 14, would increase $30/nt over the next three years.

Insiders told SteelOrbis the new plan is seen as less disruptive than an earlier version put forth by the US Trade Representative in March calling for port fees ranging from $1.5-3.5 million per Chinese ship per port call.

"The new plans mostly target larger ships," the insider said of the new proposed Chinese shipping fees. "Overall, my shipping contacts tell me the fees are not as bad as originally thought," he said. "Most lower weight ships will be exempt, and it won't really affect steel. There is also a 180-day adjustment period, so no one is going to turn into a pumpkin waiting for the steel deliveries to arrive."

May US scrap pricing seen down with increased flows into domestic yards, peak prices for finished steel noted

Thursday, 24 April 2025 19:59:33 (GMT+3) San Diego

US scrap pricing for the month of May is seen sideways to about $20/gt ($20/mt) less this week amid reports of increased scrap flows into domestic yards and as claims continue that limited US demand for finished steel has caused domestic flat and long steel pricing to peak, meaning mills might require less scrap during May supply negotiations, market insiders told SteelOrbis this week.

And, while it still remains early in the monthly scrap price assessment process, in the US Midwest, Ohio Valley prime busheling scrap is expected to settle at least $20/gt ($20/mt) less than its April counterpart.

"We're seeing better weather for scrap deliveries and increased in-bound flows into local yards," said one Midwest scrap insider. "(Lower pricing) on flows of HMS and other cut grades, are part of the continuing softness that we have seen over the last few months. As of right now, the call for Midwest cuts is sideways, while shredded scrap is seen slightly down."

The insider said the current level of industry uncertainty remains high, especially for June scrap pricing, depending on whether a recent pull back in overseas scrap market pricing continues. June is also the month when increased US scrap purchases could occur as buyers in the US South will be procuring scrap to fuel output from the new 600,000 ton per year Hybar rebar mill located in Osceola, Arkansas.

"There's so many uncertainties with the new tariff environment," the insider said. "If the demand from scrap export markets comes back, it might result in less (domestic) tons being made available, which could be supportive for US prices."

Recently, US prices for flat rolled coils have retreated as well towards $875-925/nt ($965-1,020/mt), or $43.75-46.25/cwt., about $35/nt less on the week. According to SteelOrbis data, HRC prices peaked at $950/nt ($1,047/mt), or $47.50/cwt., in mid-March and once again in early April.

"Buyers are sitting and waiting on additional HRC sales because there's just too much uncertainty in the market right now," said another flat steel insider.

Long steel markets, which use scrap as mill input, report "prices may have peaked for now," with domestic rebar on an FOB mill basis is assessed with most transactions noted at $38.00-39.50/cwt. ($760-790/nt or $838-871/mt), on average $38.75/cwt. ($775/nt or $854/mt), unchanged from seven days ago.

"Buyers are taking a very conservative approach to buying steel at the moment," said one SteelOrbis long steel insider. "With a recent decrease in purchases, domestic rebar and wire rod pricing has stayed very steady for several weeks now," he said.

Based on a $20/gt decline estimate for May, prime busheling and shredded scrap for May delivery could settle near $445-470/gt ($452-478/mt), while shredded scrap could settle near $395-400/gt ($401-406/mt). Cut grades are currently expected to settle sideways for May meaning HMS1 could settle near $365-385/gt ($371-391/mt), while P&S scrap is seen flat to April values at $401-411/gt ($407-418/mt).

And while no concrete estimates are yet available for East Coast scrap grades, following on April declines, and considering recent declines in global scrap pricing, most insiders expect domestic scrap pricing for May to reflect similar declines seen during April supply negotiations, when levels were off between $20-40/gt ($20-41/mt)